When I was growing up in Malaysia, there really was only one way to get ahead.

You started a business. You took a calculated risk. And if you succeeded in providing a product or a service that people wanted, you gained positive traction. And you reaped the long-term benefits of doing so.

Of course, succeeding in business was no easy feat. You needed determination, diligence, and vision. As well as a generous sprinkling of good luck.

Interestingly enough, I have never encountered anyone in Malaysia who made serious money by being a property investor. It just wasn’t feasible to do so.

The housing supply in the nation was plentiful. So capital growth was limited. You didn’t get much upside for putting in the work for being a landlord. For most people, it was far better to invest in a business instead.

However, when I first arrived in New Zealand, I was greatly surprised. Things were so different here. It wasn’t business that drove the agenda. Instead, it was property.

Housing was king. Plenty of Kiwis chose this as their main vehicle for growth, income, and security.

A culture shock for me? Absolutely.

A love affair with housing

Generally speaking, two forces seem to be driving Kiwi investors toward property:

- Historically, the zoning and resource-consent laws in New Zealand have made it very difficult to build housing at scale. This has created a chronic shortage of affordable homes. This, in turn, has placed upward pressure on property prices.

- Meanwhile, compliance costs and regulatory burdens have escalated over the years. Putting a tight squeeze on Kiwi businesses. Entrepreneurs face fierce headwinds. Only 37% of small companies will survive after two years. Failure, not success, is the rule here.

So, naturally enough, for many people, the path of least resistance will be property:

- If you can borrow cheaply, if you can leverage it — well, in theory, the sky is the limit.

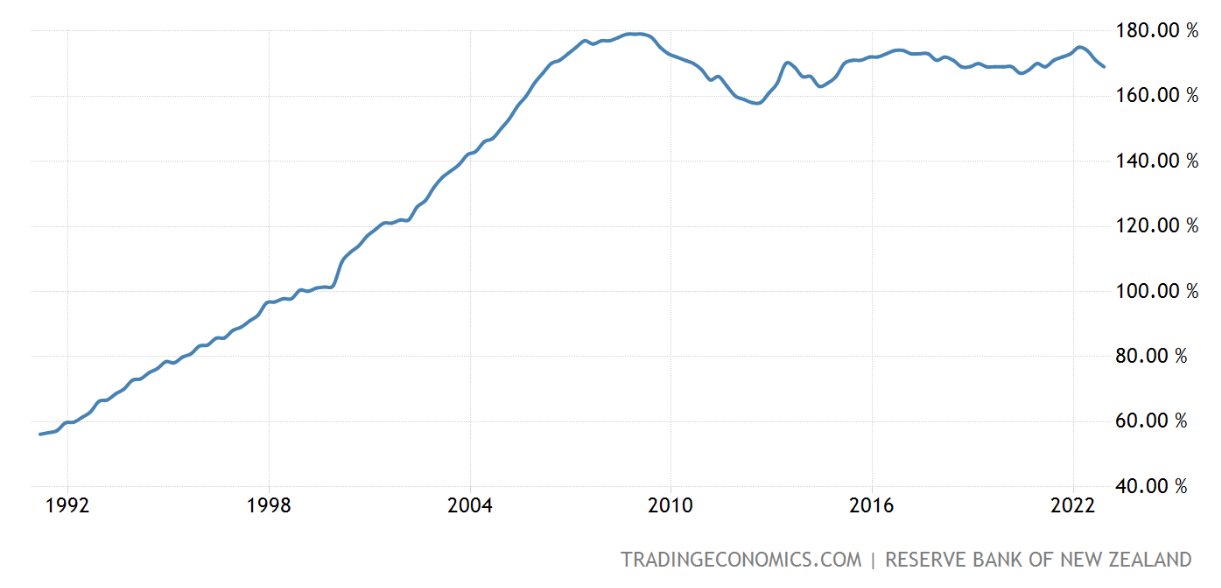

- It’s no wonder that New Zealand’s household debt has ballooned over the years. It peaked in 2022 with an astounding debt-to-income ratio of 175%.

Source: Trading Economics

Why so much debt? Well, why not?

- Kiwis have grown comfortable with large mortgages — because up until now, the reward they received in return for taking on that debt seemed pretty clear-cut.

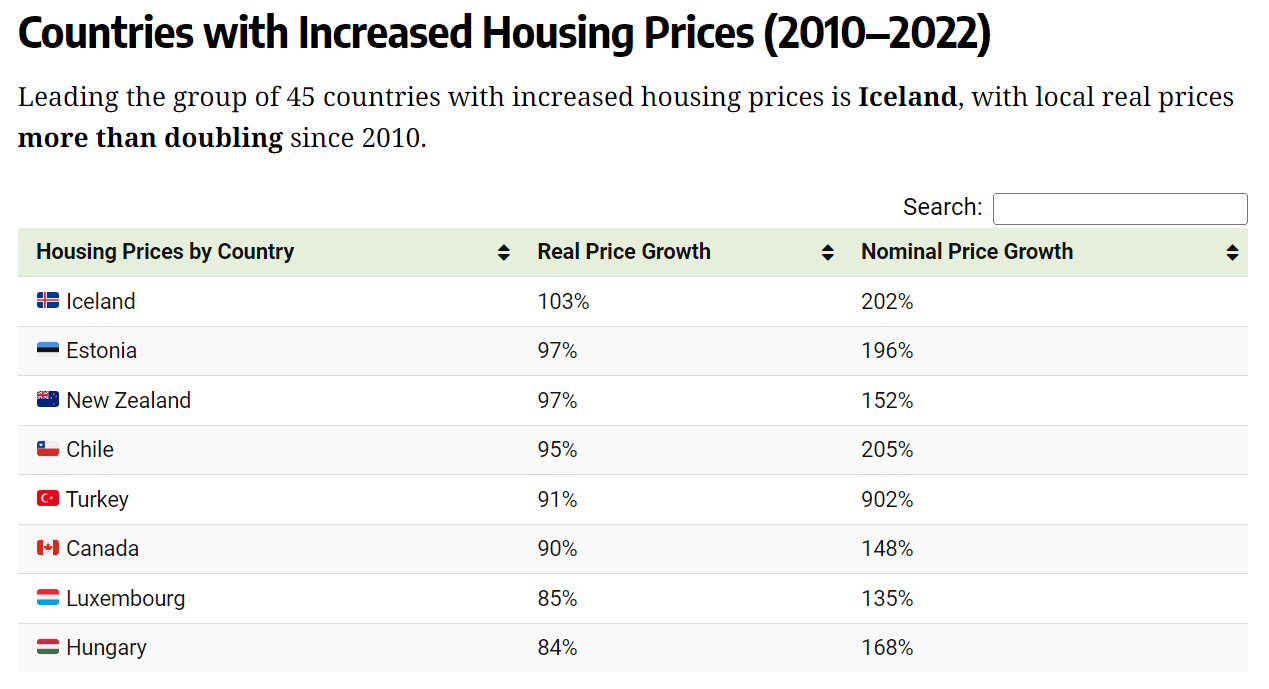

- New Zealand has one of the most expensive housing markets in the world. The surge in prices over the past decade has been dizzying:

Source: Visual Capitalist

So, you can’t blame property investors for experiencing emotional euphoria. It has reinforced certain deeply-held beliefs:

- ‘Investing in housing is safe.’

- ‘Investing in housing is secure.’

- ‘Investing in housing is risk-free.’

Unfortunately, the idea that property is risk-free is simply not true:

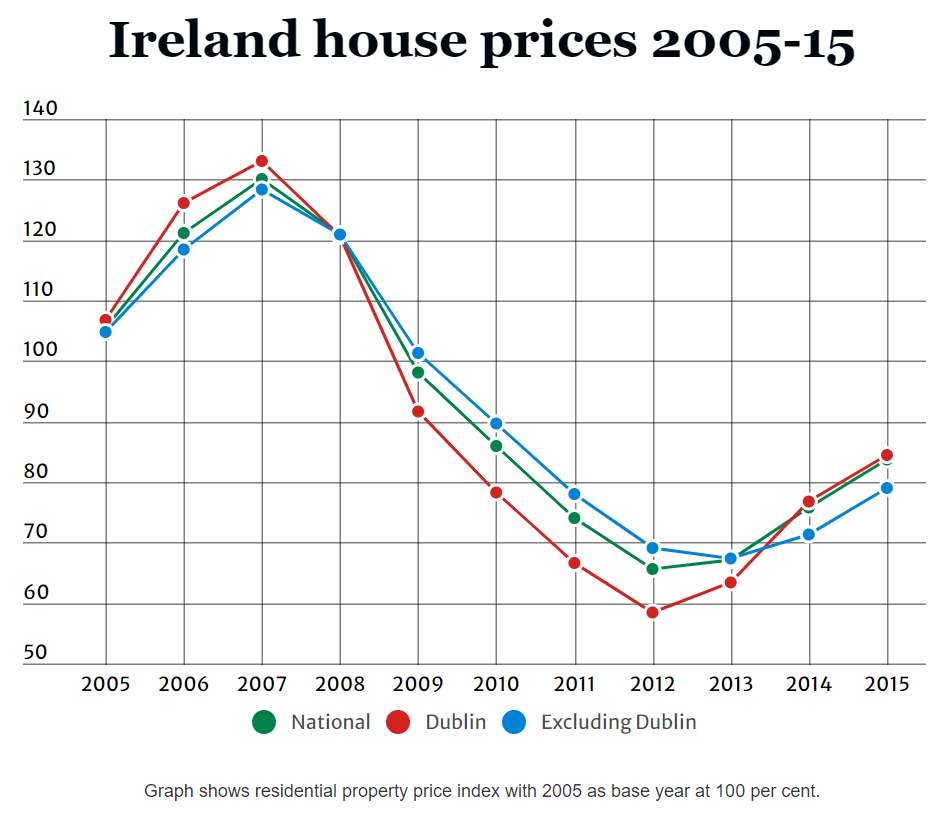

- For example, look what happened in Ireland. A real-estate bubble started to appear in the early 2000s. That’s when excessive borrowing and speculation reached a fever pitch.

- When a credit squeeze arrived, courtesy of the Global Financial Crisis, the bubble popped. This was devastating. In 2013, house prices in Dublin crashed an astonishing 54% from their peak.

- Talk to any Irish person who lived through this period. You will understand what a deeply traumatising experience this was for the Celtic Tiger.

Source: Stuff

Of course, what happened in Ireland was an extreme example of a housing meltdown. Chances are, it won’t happen in New Zealand, given that our market has very different fundamentals:

- Perhaps, in the grand scheme of things, the Reserve Bank of New Zealand has done us all a favour? They have raised the official cash rate steeply from 0.25% in August 2021 to 5.5% today.

- This has caused much anxiety and anguish. This is particularly acute among people who are deeply plugged into this ecosystem — housing developers, mortgage brokers, real-estate agents, and yes, mum-and-dad property investors.

- Let’s face it: no one likes it when the easy money is taken away. No one likes it at all. The shock of this withdrawal is even more excruciating when you realise that what we’re seeing is the steepest rate-hike cycle since 1999.

- Yes, the medicine is bitter — but, ultimately, the patient needs it. By pumping the brakes on the housing market, the Reserve Bank may have saved us all a lot more pain and grief further down the track.

- So far, from peak to trough, the Auckland housing market has experienced a correction of 27%. This is stressful, yes, but at least it’s not the 54% crash that we saw in Dublin.

Nonetheless, this financial shake-up is raising some important questions:

- Are the days of extraordinary capital growth in housing over?

- If so, does it make sense to look at the stock market as an alternative?

- How advantageous is it to invest in shares?

Comparing property with shares

Source: Speedprop Global

History can serve as our guide here. Here’s the scenario for NZ-based real estate:

- On 31 March, 2003, the median price of a New Zealand house was $200,000.

- On 31 March, 2023, the median price of a New Zealand house was $775,000.

- This represents growth of 252% in nominal terms.

- This does not assume rental return — though studies show that this may only add around 0-3% on a net basis after costs, on average.

Meanwhile, for comparison, here’s the scenario for NZ-based shares:

- On 31 March, 2003, the NZX 50 index was 1,931.61 points.

- On 31 March, 2023, the NZX 50 index was 11,884.50 points.

- This represents growth of 515.26% in nominal terms.

- This assumes the reinvestment of all dividends.

So, generally speaking, the stock market has enjoyed better growth than property. Here’s why:

- Shares provide immediate access to dynamic companies. They solve problems, provide services, create products, secure new customers.

- Shares provide instant diversification across a range of industries and geographic regions. This reduces overall risk exposure.

- Shares provide both liquidity and accessibility. This allows people at any level of income or experience to participate.

Now, of course, if you’re skilled enough to stock-pick, you can find even more value in the global market. You should consider which is better:

- Option One — A three-bedroom house in Auckland, situated in a single vulnerable location. This property may be 30% overvalued, paying a gross rental yield of around 3%.

- Option Two — A real-estate investment trust in Australia, operating over 300 childcare centres spread around the nation. This Company appears 30% undervalued, paying a gross dividend yield of almost 6%.

- Now, rationally speaking, investing in Option Two offers a clear benefit over Option One. When you can buy into a well-diversified asset *below* its fair value, you immediately gain a long-run advantage. This is a powerful force that compounds over time.

- As a shareholder, you become the joint owner of a billion-dollar company. When the Company prospers, you prosper. In my opinion, this is the best golden handshake ever.

So, what are smart investors looking for?

- Better prospects for capital growth.

- A stronger stream of passive income.

- Diversified wealth protection.

- As the economic cycle switches gears, new openings have emerged for real-estate stocks.

- In the words of Warren Buffett: ‘A market downturn doesn’t bother us. It is an opportunity to increase our ownership of great companies with great management at good prices.’

Take action now

So, right now, here’s what you need to think about:

- Is it time for you to scale up?

- It is time for you to go global?

- Is it time for you to look at property assets on the stock market?

These are big questions. Critical questions. And if they are important to you, you need to act now. Please accept my exclusive invitation.

🎯 Come join our Quantum Wealth Report.

To date, we have investigated and exposed over 100 hidden ideas. From property to energy; from artificial intelligence to cryptocurrency; we are doing a deep dive into the latest quantum trends.

These are cutting-edge insights that could change your destiny — if you have the courage and conviction to follow through.

Ask yourself: are you concerned about your family’s well-being and happiness?

Well, if you are, this is the best time to act…

Get started and receive your first Quantum Wealth Report today:

Regards,

John Ling

Analyst, Wealth Morning

(This article is general in nature and should not be construed as any financial or investment advice. To obtain financial advice for your specific situation, you should speak to an authorised Financial Advice Provider.)

John is the Chief Investment Officer at Wealth Morning. His responsibilities include trading, client service, and compliance. He is an experienced investor and portfolio manager, trading both on his own account and assisting with high net-worth clients. In addition to contributing financial and geopolitical articles to this site, John is a bestselling author in his own right. His international thrillers have appeared on the USA Today and Amazon bestseller lists.