The globalist financial media hates the Trump tariffs.

Spend any time with them and you’ll start feeling that American exceptionalism is over. American markets are destined for further drawdown. And China will carry the growth torch for the next decade.

But are these reports credible? It never fails to surprise me that analysts and traders hang on the words of journalists who seldom spend any time at a trading desk.

Their catastrophising is our opportunity. Thanks to the ‘coming doom’ of impending tariffs, we’ve found volatility to buy again.

Tariffs seem very unpopular with the MSM. Others may feel differently.

Source: Ian Jaeger / X

Watch the tax take

Tariffs are a tax on imports that go into the federal coffers. Before World War I, the federal government was significantly funded by them.

For the past few decades, the US market has been one of the most open consumer markets in the world with the lowest average tariff rates.

New Zealanders calling foul on new tariffs should consider our GST regime. This slaps 15% on all imports coming into the country. It provides 25% of our tax take.

It’s a similar situation with the VAT regime in European countries.

The view that every country in the world ought to have free access to the US is an entitled one. Market access is a privilege. Not an automatic right.

As US tariff revenue grows, it will allow for the repayment of debt, the lowering of interest payments (which are set to exceed the defence budget), and cuts to income tax.

We’re also seeing huge inflows of FDI (foreign direct investment) into the US. Since taking office on 20 January, Trump has seen nearly $2 trillion in US-based investment.

To put that in perspective, over the same period, China has received around $24 billion (about 1.2% of the American total).

Despite claims of China preparing to take the economic lead again, their tax revenue is dropping. This has come from a culmination of deflation, falling property taxes, falling income taxes –— and yes, despite tariffs on imports, falling revenue there too.

This is before the full bite of the now 20% tariff on exports to the US is felt.

Consider the counterintuitive

The US has the worst life expectancy in the G7. Over the past few decades, an open-import economy has not served the country well. As globalisation has taken manufacturing, it has also ripped out purpose from working and middle class communities.

More perniciously, it has taken the inevitable innovation that comes from the practice of making things.

I grew up amongst engineers and dairy factory workers in Taranaki. When they weren’t on the factory floor, they were innovating in their own garages. One built the first video-game console I saw.

Fonterra Whareroa Factory near Hawera, South Taranaki. ‘Kiwi Dairy Factory’ in my day.

Source: Wikimedia Commons

Restoring manufacturing means bringing back innovation ecosystems.

In this part of the world, we need a strong America that can lead in the Pacific. It is a defence partner to Australia, and via that — though more tenuously — to New Zealand also.

Without American strength, Australasia is somewhat defenceless.

Listen to the deal

Trump is not saying a European automaker cannot, for example, sell cars into America.

He is saying if you make your Mercedes in Germany, it will face a 25% tariff.

If you make that in Alabama (where they have a large plant), it will not.

Mercedes-Benz US International Plant located in Tuscaloosa County, Alabama.

Source: The George F. Landegger Collection of Alabama Photographs in Carol M. Highsmith’s America, Library of Congress, Prints and Photographs Division

Trump is also saying if you want to make a deal on some of the trade barriers American firms face in your market, we can do a deal too.

For example, American firms face considerable difficulty accessing European markets, not only due to tariff barriers but via other hurdles such as minimum global taxes and complex regulations and standards.

Consider the long run

Yes, tariffs will disrupt established global trade flows. However, once they are settled (or negotiated), they become a one-off cost that markets quickly adjust to.

There may be some short to medium-term market drawdown. In our view, if this presents some genuine value, it’s likely a good time to buy.

The immediate aftermath of tariffs is also likely to speed up interest-rate cuts in markets outside the US as they try to recalibrate. Lowering the ECB rate, for example, is likely to weaken the euro against the US dollar. That helps to soften some of the tariff blow.

We have also been here before in the first Trump administration.

What we saw there was initial volatility and opportunity. Then Biden kept the tariffs on. The market adjusted, and we still had a fantastic run-up of the S&P 500 in 2023 and 2024.

So, when you read or hear some bad Trump/tariff news, try and strip back to the author’s intention and experience. Naturally, many are sympathetic to the shudders that tremor across businesses in Europe and Asia. Some to the vocal Left with their hair on fire.

We are traders and global investors. So, yes, we’re biased to long equities. But we have conviction that over the long run that will serve us well.

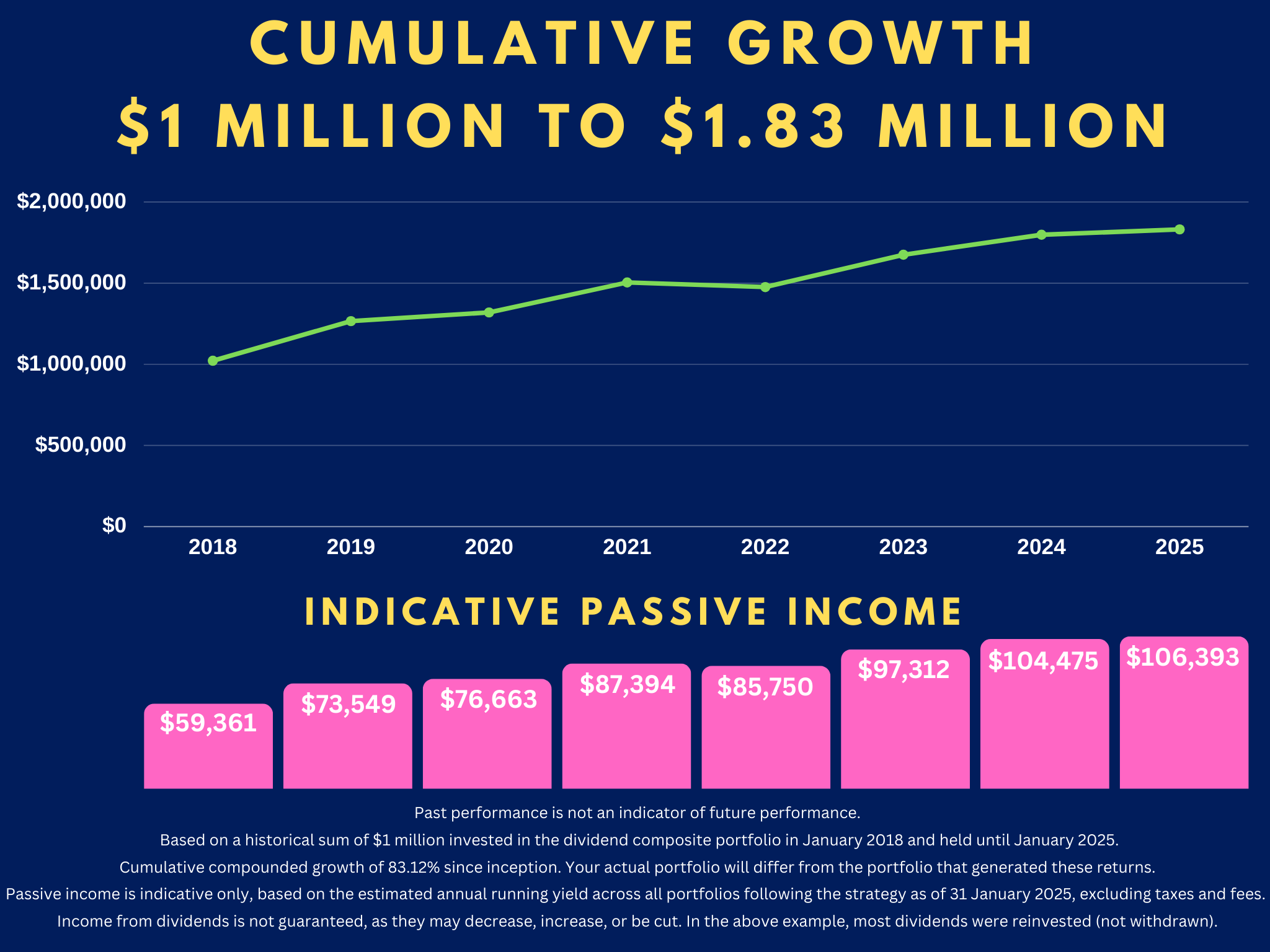

Are you looking for global opportunity?

We build diversified and income-rich portfolios for our Eligible and Wholesale Clients.

Do you have previous experience in investing?

Are you a sophisticated investor?

Or have you built significant wealth?

All these characteristics could qualify you as an Eligible or Wholesale Investor for a managed account under our strategy. The assets remain in your name, and you retain full ownership and custody of your assets.

We are currently offering free consultations on this opportunity.

Regards,

Simon Angelo

Editor, Wealth Morning

(This article is the author’s personal opinion and commentary only. It is general in nature and should not be construed as any financial or investment advice. Please contact a licensed Financial Advice Provider to discuss your personal situation. Wealth Morning offers Managed Account Services for Wholesale or Eligible investors as defined in the Financial Markets Conduct Act 2013.)

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.