Monthly, we update our wholesale investors on what’s happening in the market. Running what’s probably the only late-night trading desk from New Zealand, we’re well-positioned to feel the pulse of the market’s direction.

June saw one of the biggest mid-month dips we’ve seen in a long time.

The swing to the right in the EU elections took the market by surprise. Then the president of France dissolved the country’s parliament and called elections for the summer.

This event proves how skittish financial markets can be. They crave certainty. Nothing must upset the apple cart of smooth growth.

This negativity pushed European stock prices down. But we felt that this was just emotion. Temporary and fleeting. After all, none of this would have much effect on our set of businesses. So we bought the dip. And in hindsight, it was a good thing that we did.

Later, polls suggested that a primary reason the French were moving to the right might be economic issues. According to an IPSOS survey: ‘The National Rally is seen as the most trustworthy when it comes to managing the economy and public finances.’

The Bardella bump

The market turned again, embracing a happier mood. Stock prices recovered and climbed. So, by buying the dip, we had captured some upside. Positioning our portfolios for growth and income.

This is a constant reminder that the market misprices assets on uncertainty. And that many investors consider it a moral beast, when rather it is ravenous wealth whore ready to reprice on a sniff of profit.

Yes, I do understand concerns around political instability. I remember 2017 very well. I was staying near a French housing estate the last time Marine Le Pen jumped in the polls. Several cars were torched. Our host told us in no uncertain terms to order dinner in.

Indeed, parts of Europe can present quite a juxtaposition. Genteel paddocks on one side. Blocks of social housing on the other.

Source: Author photo / Wikimedia

But, quite often, the scary news is just that: scary news.

It’s amplified. Exaggerated. Oversold.

It doesn’t accurately reflect the true situation.

Nonetheless, we understand that the fear is there to give us an opening. An opportunity.

We are value investors. And we scour the world for quality businesses priced below their intrinsic value. Businesses that can provide — as per our Client Proposal — ‘global diversification, income, capital preservation and growth.’

Here’s an explanation of how we seek these components at the trading desk:

1) Global diversification

Most of our clients have the lion’s share of their wealth in New Zealand, especially in property.

The NZX is a small market. It seems expensive when you look at earnings multiples. Picked bare after waves of global money.

But the resounding reason we don’t focus on it is that it lacks depth of industry.

There are no semiconductor firms, automakers, significant commodity, or global financial businesses.

Instead, we seek developed markets where transparency and value are evident. We look for growth prospects and good income yields.

In particular, we target sectors projected to outperform over the next decade.

These sectors include:

- AI (artificial intelligence)

- Personal mobility

- Leading-edge healthcare

- Fintech (financial technology)

- Mining

- Counter-cycle real estate

2) Income

As at June 2024, the projected income on the largest portfolio of dividend stocks under our strategy sits at 6.56%. This is entirely from dividends.

On $1,000,000 of dividend-paying stocks, that projects an annual passive income of $65,600 (excluding any taxes and fees).

What has happened here is that many of the dividends have increased from the time of purchasing the positions, often ahead of inflation. Of course, dividends are not guaranteed. They can get cut in tough times too.

Now, some may argue you give up a degree of growth to earn this income — since companies are reinvesting less profit. There is the counter-argument that the ability to pay a reliable dividend reinforces the strength of the business. While sector and business growth drives share-price growth.

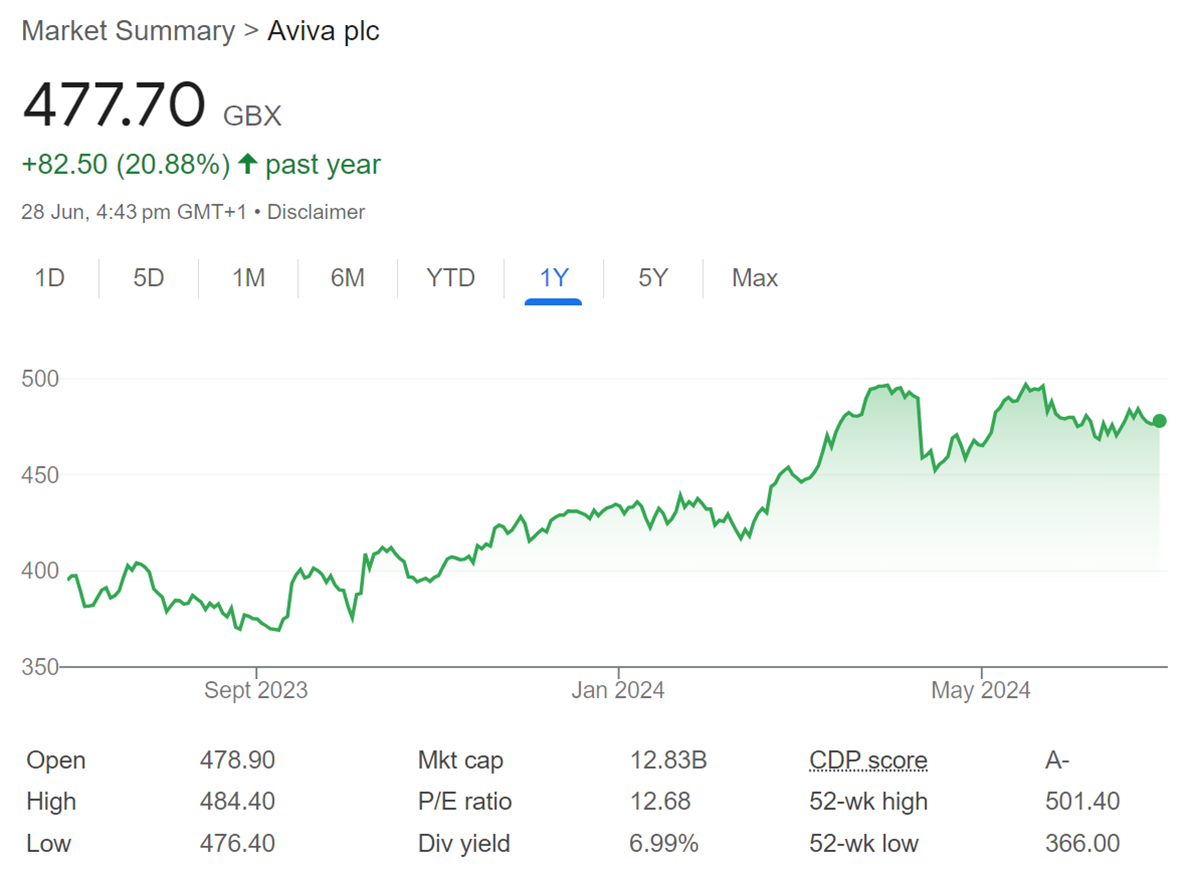

For example, one of our picks — the giant UK insurer Aviva [LSE:AV.] — has managed both stock-price growth on a keen valuation and an excellent dividend yield:

Source: Google Finance

3) Capital preservation

Warren Buffett made a couple of memorable remarks that it pays to keep front of mind:

‘Rule No. 1: Never lose money. Rule No. 2: Never forget Rule No. 1.’

‘If the business does well, the stock eventually follows.’

Stock markets are dynamic markets where businesses get priced every day. When you invest in businesses, by definition, you take on a degree of risk. Not all will flourish or even survive. Often due to events outside anyone’s control.

Over the medium to long-term, our strategy seeks to limit risk and protect wealth by:

- Generally investing in larger concerns that have identifiable ownership of good-quality undervalued property.

- Mainly restricting our remit to developed country markets, keeping emerging countries and regions to speculative allocations only (typically less than 4% of a portfolio).

- Diversifying (but not ‘diworsifying’) across enough positions and sectors to protect portfolios in downturns. Excepting a few very strong opportunities, we generally have no more than 8% in any one position.

- Generally looking for long-term debt levels below 40%, with the ability to go to ~45% for exceptional recovery opportunities.

4) Growth

We target 15% overall.

This was certainly achievable last year when we reported almost 20% across the composite portfolio. Of course, when you’re also targeting entry-yield dividends of 5%, it is conceivable that income will come to generate a significant part of your return.

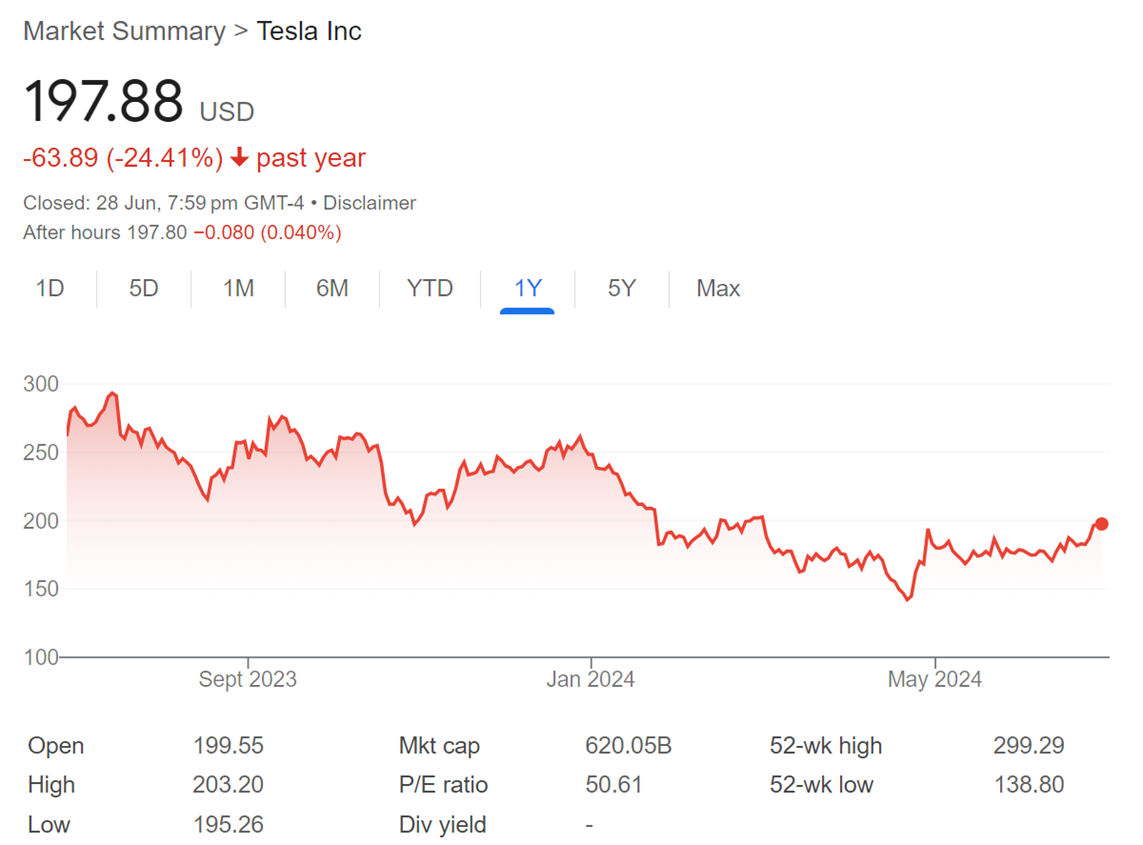

If I were to level criticism at our strategy, it would be that we invested little in key technology-based growth drivers like Tesla [NASDAQ:TSLA] or Nvidia [NASDAQ:NVDA]. Companies that exhibit rapid growth yet do not pay any income.

But I would counter that criticism with the fact that heavy ‘risk-on’ strategies can devastate portfolios when the tide turns.

While I admire Elon Musk and the Tesla story, when we looked at it last year, it was simply too expensive. This has not aged well for those who felt otherwise:

Source: Google Finance

A P/E in the 40s may make Tesla somewhat more attractive. But there would still have to be a certain path to very rapid growth.

Nvidia has been a different story. Very fast growth. Very high P/E. While it has been tempting, research has also revealed much cheaper semiconductor companies that could, in time, cut its lunch.

This is not to say that we avoid high-growth or speculative positions entirely.

In our larger portfolios, we do have a few ‘up to 2%’ places for breakout growth opportunities. No dividend. High risk. But potential 10-baggers. Should they not work out, the ballast of a larger defensive-focused portfolio protects the overall return.

At the moment, such interesting prospects include Joby Aviation [NYSE:JOBY]. A frontrunner in personal mobility — in particular, the potentially revolutionary new industry of airborne rideshare.

Joby S4 at Japan Mobility Show last year. Source: Wikimedia Commons

Though the bulk of our strategy resonates with another Buffett aphorism:

‘I don’t look to jump over 7-foot bars. I look around for 1-foot bars that I can step over.’

Many investors think the stock market will boom when the economy rebounds. In actual fact, some of the more meaningful sector climbs come about when the wider economy is sluggish and central banks are ready to cut interest rates. (Like now — or at least over the next year).

Carefully selected real estate can do very well when bought before and during such times.

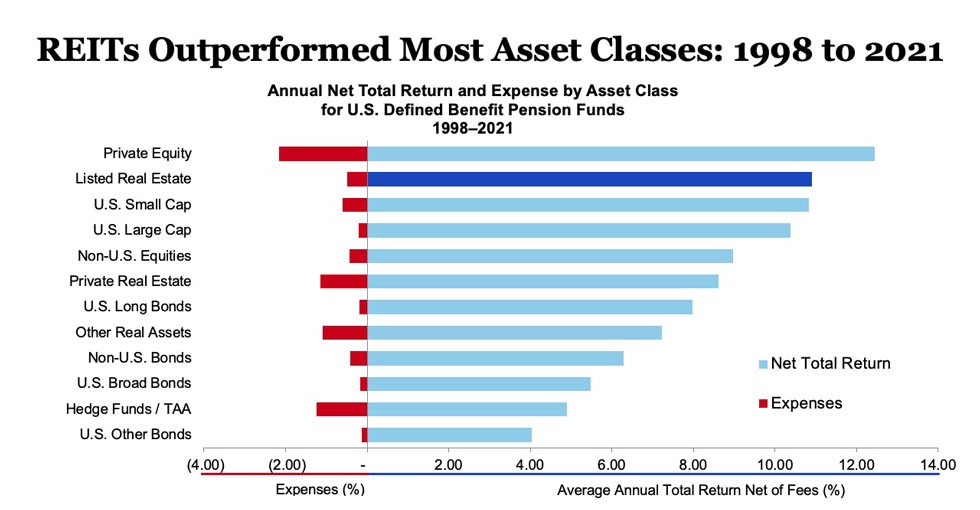

Evidence since 1998 indicates that REITs (Listed Real Estate) have outperformed both private real-estate investments and S&P 500 stocks:

Source: Nareit

This chart is focused on US REITs and does not reflect some of the interest-rate pain that occurred after 2021. But it is important to point out that REITs tend to do best when interest rates soften. This occurred for long stretches between 1998 to 2021.

We make no apology for our strong weighting on handpicked real estate around the world. When combined with distributions (dividend yield) and counter-cycle opportunity, it should reward patient investors.

At this point, quality real estate provides a good ‘1-foot-bar’ component in our long-run strategy.

Of course, there will be ups and downs along the way.

Managed Account performance*

For the month of June 2024, we were down 1.11% across the composite portfolio (total aggregate TWR return across all portfolios following the strategy).

Our MSCI EAFE benchmark was down 2.59%.

Our YTD performance is 3.30% (January to June 2024), or 6.60% on an annualised basis.

Our average annualised return since inception is 13.03% p.a.

Please see our performance chart for more details.

Our vision

Wealth Morning Managed Accounts is a premium, transparent solution for Wholesale and Eligible Investors.

We scour developed markets for the world’s best quality businesses. Selecting a small number of carefully researched positions on a zero-regret basis.

When we buy shares in a business, we email our wholesale clients and tell them the precise reasons why. And we look to build robust, defensive, and income-rich portfolios to secure our clients’ financial freedom over the long run.

Our vision is to be this country’s leading trading desk focused on global value. Providing our wholesale clients a managed portfolio solution in their own account.

Regards,

Simon Angelo

Editor, Wealth Morning

*Past performance is not an indicator for future performance. Your actual portfolio will differ from the composite portfolio mentioned. The information contained in this document does not constitute an offer to sell or a solicitation to buy an investment, nor should it be construed as investment advice. Wealth Morning Managed Accounts are available to Eligible Investors and Wholesale Investors (not to Retail Investors) as defined in the Financial Markets Conduct Act (2013).

🎯 Our Exclusive Managed Account Service

👉 Secure Your Place on Our Waiting List Today

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.