Do you attend any Board or Shareholder meetings?

I’ve had a few recently. And I’ve come across a certain kind of individual. One that makes me deeply suspicious.

They drive up in their EV. Then have much to say on the current themes of our time. Diversity. Inclusion. Climate. Gender rights. ESG (environmental, social, and governance objectives in investing).

Now, these things are well and good. No decent person wants to promote unfairness or pollution.

But I’m suspicious, because more often than not, I find myself sitting there and asking: ‘Are your messianic claims on these themes actually adding value? Or are you instead virtue-signalling yourself some points in the popularity contest of the day?’

The masks are off now. And their friends in mainstream politics and media face an audience that is growing wary or dispersing.

It’s easy to gloss over things. I like to see leaders stand up for facts. Provide the research. And say, ‘Well, if you disagree, feel free to come at me.’

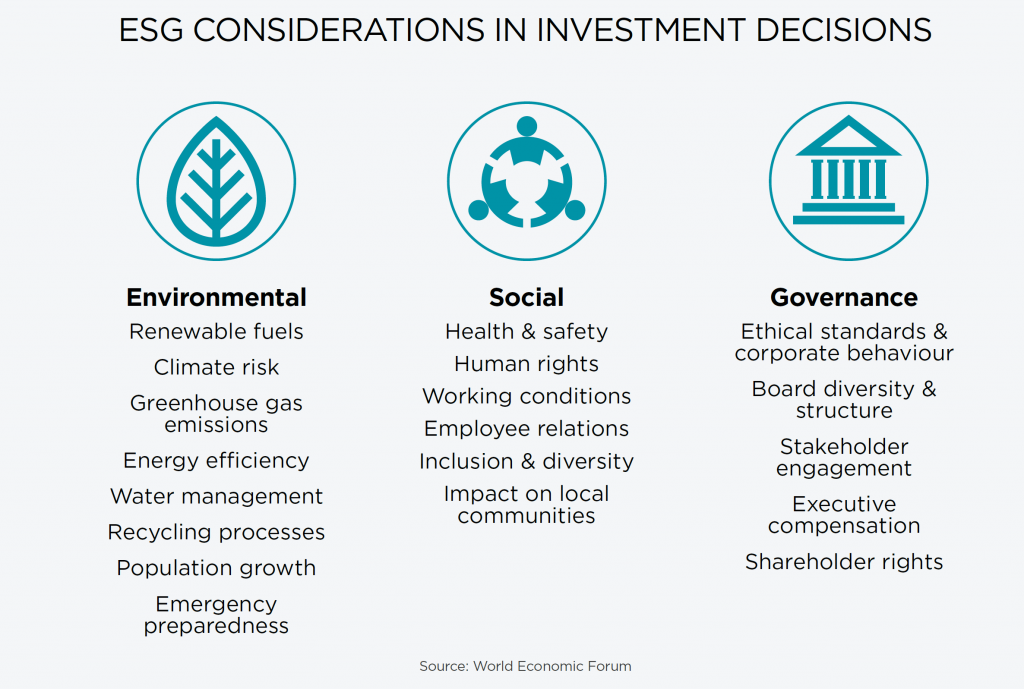

ESG investors

These days, you can find specific funds that are labelled ‘ESG’.

All stocks selected for inclusion in an ESG fund must contain companies that score highly on environmental, social, and governance criteria. This is pretty wide-ranging, covering everything from diversity in the boardroom to emissions.

Last year, over $2.7 trillion in investment funds found its way into ESG exchange-traded funds alone. An amount equal to the entire GDP of the UK.

ESG has been popular. More and more investors are starting to request it for their portfolio strategy.

Unfortunately, much of the research to date doesn’t appear to paint ESG in such a great light.

Not only has it been underperforming other strategies, many so-called ESG companies have not been delivering on their moral promise.

Sure, you may expect ESG investments to perform a bit below the rest of the market. They can’t profit from areas like fossil fuels, for instance.

But the actual underperformance is significant:

- According to Bloomberg, Global ESG funds have underperformed the broader market over the past five years by an average of around –2.6% per year.

- To put that into perspective, an investor with $100,000 in an ESG fund from 2017 until today would have around $17,200 less than another investor in a broad market fund.

- I know of at least one fund manager here in New Zealand that has withdrawn their ESG fund altogether.

All right, but perhaps –2.6% a year is a reasonable price to pay for ‘saving the planet’?

Unfortunately, the credentials of many ESG companies have been found lacking on various fronts.

A recent paper from researchers at Columbia University and the London School of Economics compared the ESG record of companies in 147 ESG portfolios vs 2,428 in non-ESG portfolios.

They found that the supposedly ESG companies had worse compliance records for labour and environmental regulations.

It is hard to fathom this. But, as a wholesale money manager, I can see where the discrepancy may arise.

In our case, we do not have a specific ESG overlay. That would require significant investment of research time into scoring every single company we analyse. Most likely, we’d have to rely on shortcuts — i.e. companies saying they are sustainable. In many cases, that would be difficult or burdensome to verify.

Instead, we simply focus on quality and end results. Quality businesses run by quality people with strong ethics.

Maybe, in this way, ESG is somewhat redundant.

Businesses that are operating with integrity already meet many of the criteria. Those that proclaim ESG credentials — machinated by nebulous, impractical policies to score well — may not score so well in the real world.

In America, the tide is now turning against ESG for this reason.

Ron DeSantis vs ESG

Florida Governor Ron DeSantis has become popular in the US for his war against things he considers ‘woke’.

So much so that many Republicans are hoping he may run for president in 2024.

Warrior against the woke: Ron DeSantis. Source: Florida Phoenix / Facebook

One of Ron’s recent targets has been ESG investors.

In August 2022, DeSantis, along with his fellow Trustees of the State Board of Administration (SBA), passed a new resolution. This directed ‘the state of Florida’s fund managers to invest state funds in a manner that prioritizes the highest return on investment for Florida’s taxpayers and retirees without considering the ideological agenda of the environmental, social, and corporate governance (ESG) movement’.

That might seem a little harsh. Anti-Biden, perhaps, whose administration has encouraged ESG investing.

But from where I’m standing, there are no grounds for Florida’s taxpayers to sacrifice return by being forced to consider criteria that do not always stack up in the real world.

Yet the question is this: wouldn’t ESG considerations help the environment?

Beware of shortcuts that bypass the truth

Any investment decision should be robust and based on high conviction. You need research to support a decision to buy. Or to avoid a position.

For example, one area I’ve not managed to get conviction on is EVs. And the sizeable rebates many governments currently offer to incentivise them.

Many people I know are now switching to EVs. Companies focused on them may score highly on the ESG front.

I did the math myself on this when looking for a second car.

Rich friends get Teslas — and I can see the attraction. Those wanting to spend less: Nissan Leafs. And those with dubious taste: the startlingly ugly MG EV (in my opinion).

Now, EVs are brilliant on urban roads, since while driving they produce zero emissions. Wonderful.

But that is not the whole story. You need to drill down to the total energy mix across the life cycle of the vehicle:

- A large-scale study in Austria found that ‘a mid-sized electric passenger car in Germany must drive 219,000 km before it starts outperforming the corresponding diesel car for CO2’.

- On average, most passenger cars in Europe last for only 180,000 km. But for EVs, the situation is more unpropitious since EV batteries don’t last long enough to achieve anything like that distance in the first place.

- As strange as it may seem, yes, running my BlueTEC diesel Mercedes for another 10 years and 100,000 km might be better for the environment than buying a new EV.

Of course, this is just based on one study and reflective of the German electricity mix.

Yet if you track the production of a new EV and its battery, the mining processes and supply chain alone generate a lot more CO2.

A review of more than 50 studies has found that embodied emissions to fabricate a single EV battery ranged from 8 to 20 tons of CO2. At the high end, that is almost as much CO2 as is produced over the lifetime of fuel burned by an efficient conventional car.

But these emissions are hidden. They occur before the EV is even delivered to the consumer. And may not be picked up in ESG analysis of revenue.

Further, Amnesty International has flagged a further concern that negates ESG claims. It says ‘human rights abuses, including the use of child labour, in the extraction of minerals, like cobalt, used to make the batteries that power EVs is undermining ethical claims about the cars.’

This is something that needs to be looked at more closely.

While improvements in battery production and recycling are mitigating production emissions, I’d like to review more investments in other technologies that are not so dependent on the mining aspect.

Toyota is one manufacturer hedging its bets with EVs, investing more into other fuel options such as hydrogen.

Then there’s the energy mix.

Here in New Zealand, in winter, our grid barely copes with demand and must burn coal to keep the lights on and cars charged. If EVs are to become not 1% of the vehicle fleet (as they are now in Auckland) but 50%, it follows we’ll need far more energy.

One thing I’ve learnt over the years in investing and working with people is this: things are sometimes not what they seem. You need to tear into the layers and find what is at the core.

And from what I’ve seen thus far, the core of a few so-called ‘ESG’ investments may well be rotten.

Regards,

Simon Angelo

Editor, Wealth Morning

(This article is general in nature and should not be construed as any financial or investment advice. To obtain guidance for your specific situation, please seek independent financial advice.)

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.