This question is on many people’s minds at the moment…and rightfully so.

Will Mainfreight [NZX:MFT] be the first NZX-listed stock to reach $100 per share? Or has it hit its price ceiling? In other words, are we too late to buy?

From the viewpoint of a potential investor in the company, let’s take a deep dive into the risks and returns that Mainfreight stock offers in order to make our best estimate.

Who is Mainfreight Limited?

Source: Mainfreight

Mainfreight is New Zealand’s premier freight logistics company.

They command a domestic market share of 45% in transport, and 30% in supply chain logistics.

The company provides international services through more than 165 branches worldwide.

These services include:

- Freight forwarding by road, rail, and sea.

- Handling of hazardous goods.

- Managed warehousing.

- Customs clearance and domestic distribution.

Now, let’s take a look at some relevant data in order to assess Mainfreight’s financial health:

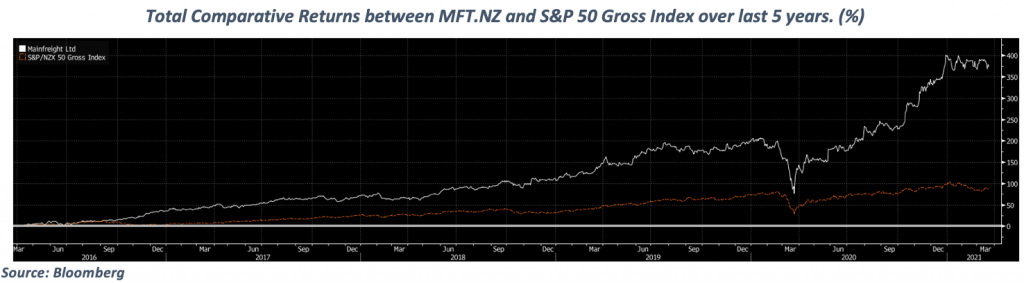

Source: Bloomberg

Mainfreight has performed fantastically in recent history.

So good, in fact, that they have managed to yield a total return of 372.77% over the last five years.

Comparatively, the NZ benchmark index — the S&P/NZX Gross Index — has returned 86.69% over the same period.

We can see that Mainfreight has set a trend for performing above the market portfolio.

Note the dip around March 2020 for both lines.

This was during the Covid-19 market crash. Mainfreight has made a spectacular recovery, and total returns seem to have benefitted from the crash. A good sign, off the bat, in case more lockdowns occur in the future.

But now look at the returns so far in 2021.

It looks as though growth has reached a plateau.

Compared to the similar state of the benchmark index, it is most likely market-related.

Insider holdings

Source: Yahoo Finance

Insider holdings make up 19.66% of shares outstanding.

On December 21st 2020, Company founder Bruce Plested purchased 100,000 shares @ $62.3 per share.

This is a promising sign, as it implies that senior managers may have a bright outlook on future performance.

It may also be good news for current holders of the stock. It assures them that the management incentive to increase share price is there.

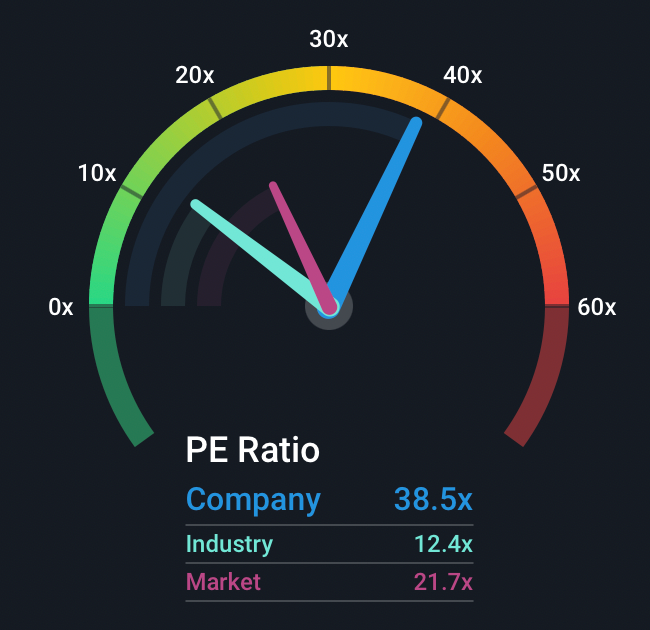

Price to earnings

Source: Simply Wall St

A point of concern that potential investors have with Mainfreight right now is its P/E ratio.

- They currently have a P/E ratio of 38.5x, which is much higher than the GICS industry average of 12.4x.

- The P/E ratio tells us that investors are willing to pay $38.6 for every dollar that Mainfreight earns.

When people see a high P/E ratio, especially relative to the industry average, they are quick to assume that the stock is overpriced.

However, outside of simple earnings, it’s important to understand that there are a myriad of factors that can influence the P/E ratio of a company.

For example, it is somewhat due to the expectation that investors have on the future growth of the company.

Historically, Mainfreight has boasted exceptional returns and consistent growth over the years. Investors may be speculating that this will continue in the future. This obviously translates to a greater willingness to invest in a more expensive company.

A useful comparison might be against one of the world’s market leaders in the logistics space. Deutsche Post DHL Group [ETR:DPW] trades at a P/E of around 19 and provides a more globally diversified business.

In March, DHL reported its 2020 full-year results. Revenue had increased 5.5% year on year to €66.8 billion.

In comparison, Mainfreight reported half-year results to 30 September 2020 with revenue of $1.609 billion (up 7.2%).

Mainfreight appears a smaller, faster-growing operation. But investors ought to question whether this sprightlier pace of growth (for the time being) ought to value the company at more than twice that of DHL (by P/E).

Vaccinated against Covid-19 (so to speak)

Mainfreight has been classified as an ‘essential service provider’ following the rise of the Covid-19 pandemic.

This has been massive for Mainfreight. It has allowed them to continue operating at near-full capacity despite the economic downturn caused by the virus.

Following suit with the economy, Mainfreight sustained decreased growth and revenue. This was especially true at the start of the panic. However, the quick rebound in performance is proof of Mainfreight’s fantastic management and ability to react to uncertain market conditions.

Going forward in a post-Covid world, it is comforting to know that Mainfreight’s services will always be in demand. Especially when this whole fiasco blows over and people are wanting to spend their hard-earned cash. I imagine that there will be a lot of goods that need to be moved from A to B.

Low net margins

Despite the potential upside for the Company, risk factors still loom large.

- Mainfreight has quite a low net margin percentage — at 5.26%. Though this has grown from around 4% over the past five years.

- Net margin is the percentage of revenue that will be realised as profit, subtracting expenses.

- It is clear that it costs a lot of money to finance Mainfreight’s operations. Think about the cost of maintaining cargo ships and planes, let alone the cost of oil needed to run them.

For now, the profit margin is not an issue as they continue to increase revenue and profits each year. However, a low profit margin means that their profitability could be at risk.

Possible embargos, policies, and tax hikes could have dire effects on Mainfreight’s profitability — especially if these situations result in revenue going down or expenses going up.

There is also the risk of competition which would pressure already tight margins. Including potential competition from large and well-capitalised players like DHL.

Another question would be about oil. Mainfreight relies heavily on the cost of this finite commodity to operate their business.

With the global economy in recovery mode, on top of OPEC limits from the pandemic, we have seen rising oil prices this year.

With already slim margins, an increase in oil price could drastically impact their profitability in future, all things being equal.

High debt financing

Following the Covid-19 pandemic, Mainfreight was forced to take on a lot of long-term debt in order to finance their operations.

- Net debt-to-equity was 15.56% in 2019.

- Following the Covid scare, net debt-to-equity spiked to 81.16%.

- This is important to note, as a high level of debt is synonymous with a higher level of risk.

- However, it should be said that financing with debt can actually be cheaper than financing with equity, especially with the low interest rates that we have right now.

What is truly important is Mainfreight’s ability to service this debt while maintaining ample capital in order to continue growth and pay short-term obligations.

Mainfreight’s current ratio of 1.1 suggests that it will have no problem in paying off its short-term debt obligations.

In terms of its long-term debt, it seems as though Mainfreight is efficiently using it to benefit the company. This was illustrated in its growth over the last year.

Increase in earnings appears enough to service their future obligations for now. If not, then they have enough assets to cover the debt if needed.

Their current debt-to-asset ratio is 39.1%.

Future growth potential

The biggest question investors have is whether Mainfreight can continue to grow sustainably in the future.

Although Mainfreight manages to consistently perform above the market, we can only take past performance at face value. It does not guarantee that Mainfreight will continue to grow at such a rate in the future.

As long as they continue to expand their asset base and network globally, then I am sure that they can continue their current growth trend.

They currently have a retention rate of 62.7%. This refers to the percentage of net income that Mainfreight is retaining to finance company growth.

This high rate, mixed with respectable earnings growth each year, signals that Mainfreight is making efficient use of its profits by reinvesting in its own operations.

Again, Mainfreight commands a 45% market share in the New Zealand logistics industry.

Domestically, they are the largest player by far.

However, the narrative is far different on the global scale.

This is where some risk comes in.

- As Mainfreight continues to expand globally, they will surely attract the attention of some of the world’s major logistics players, such as DHL [ETR:DPW] and Kuehne + Nagel [SWX.KNIN].

- If they begin to suspect that Mainfreight is eating into their market share, then they may take some competitive action.

- An example being the possibility of stealing away Mainfreight’s clients by undercutting them on service prices.

- This is a move that could be disastrous for Mainfreight as they rely heavily on volume due to their low net margins.

- This is a valid threat, considering the huge network and global presence of these larger competitors.

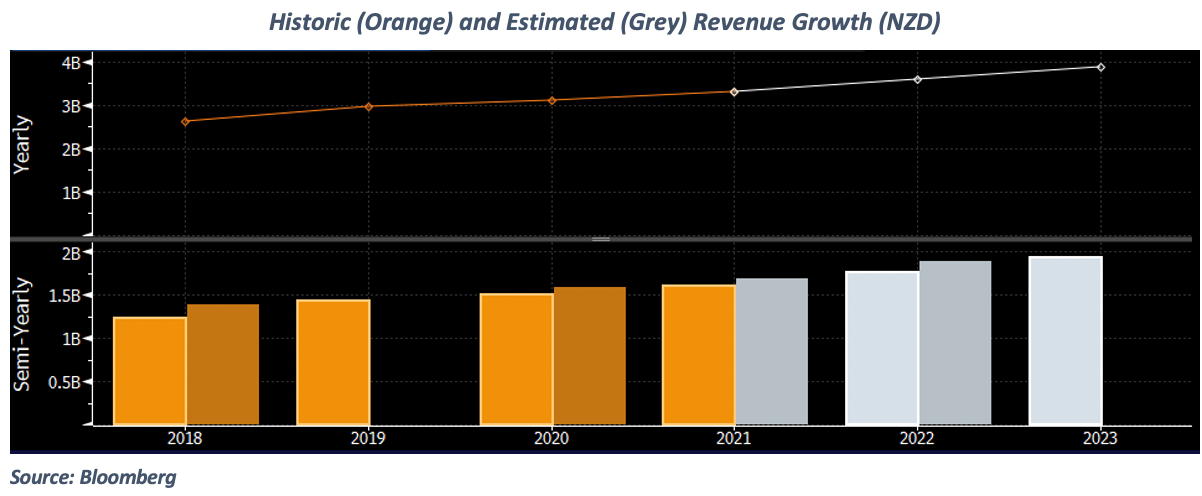

Despite the risks, analysts at Bloomberg have forecasted revenue for Mainfreight to continue the growth trend for at least the next two years:

Conclusion

All in all, it is tough to say whether it is too late for potential investors to hop on the Mainfreight growth train.

At the price that it is now, some analysts believe that the stock is overvalued.

Yet many believe that it has a lot more to offer investors.

It is up to you, the individual investor, to assess your risk tolerance and decide whether it is worth it or not to find out.

I personally believe that Mainfreight is here to stay for a long time. It exists in a growth area of the economy and has a proven history of revenue growth.

If the management can continue to bring in high quality income while keeping expenses and debt in check, then I think that they are truly on their way toward their 100-year vision.

Regards,

Samael Knaap

Analyst, Wealth Morning

Sam is an intern analyst at Wealth Morning. He is currently completing his major in finance, while juggling his roles as President of the Massey University Investment Club and student fund manager. He won the Investment Club stock challenge, where he achieved a return of 44% over a 3-month period. Furthermore, he has received the INFINZ scholarship award for being the top 3rd year finance student in 2020. His role involves contributing research and writing financial reports for Wealth Morning’s readers.