I’ve never been one for dire predictions. But I could rattle off more than a few warning signs out there on the horizon.

The price of gold continues to go up. Bond yields are falling. The return on German bonds have even dipped back into the red…again. That means you now have to pay to hold German debt. The much talked about US yield curve is flattening out, and in some cases is inverted.

Maybe you’re desensitised to all this, though.

We’ve heard doom and gloom for weeks from the pundits. And yet, the world continues to spin on its axis.

Maybe a more powerful signal then, is one of Australia’s oldest investment partnerships shutting its doors. Yes, JCP — the once $10 billion fund — is selling off assets and returning cash to investors.

Why close the doors now? I think you could take a pretty good stab at that one…

It’s not if but when

It’s becoming extremely hard to pick winners. Especially if you’ve got $10 billion to put to work. And because winners are so few and far between, JCP has seen their fee revenue come under pressure.

You see, JCP makes their money by charging clients a fee. A fee for managing their capital and a fee if they have great performance.

Yet lately it’s been harder to come by the second, the first has struggled as well.

JCP’s long only strategy returned 5.7% a year in the past three years, Mercer reminds us. It barely beats the rise of gold, which is up 5% annually over the last three years.

JCP is also not the only fund to fall recently. The Australian Financial Review (AFR) explains:

‘JCP’s move follows the downfall of other big and well-known Australian funds management teams in recent years, including Colonial First State Global Asset Management’s “core” team, AMP Capital’s active equities team, Arnhem Investment Management and most recently Janus Henderson’s Australian equity team.

‘In their place are Australia’s big industry funds, some of who have established powerful internal equities teams, global fund managers like Magellan and a bunch of passive and quant-based funds.’

It seems pretty clear what the problem is…stock prices are just too high. Valuations are stretched and it’s becoming harder to find a bargain in the top end of the market.

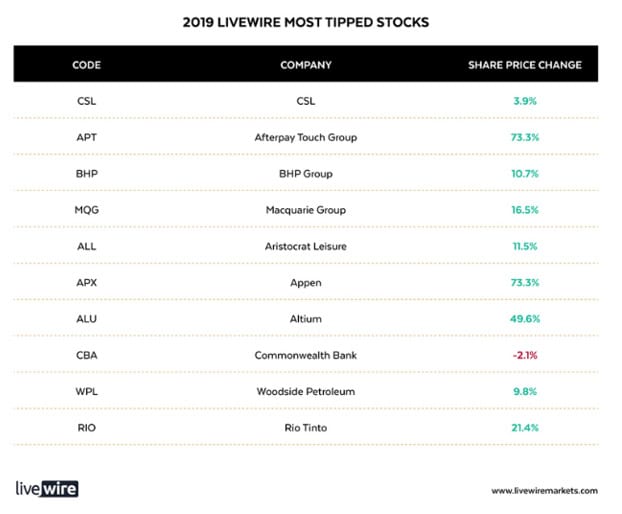

But for some, this isn’t a problem. Take a look at Livewire’s (an outlet for fundies to vent) most tipped stocks for 2019. There’s more than a few expensive names on there…

Source: Livewire Markets

And this is the aim now.

Fundies aren’t looking for bargains. They’re looking for momentum plays. Stocks which have been rising and could continue to rise as they beat sales or earnings expectations by a few percent each quarter. [openx slug=inpost]

Amazon is yet another great example.

It’s a company that once had a dominant position in books, DVDs and CDs. Now, they try to do everything. If it wasn’t hard enough winning US retail, Amazon decided to jump into multiple countries, spreading themselves thin.

At the same time, they couldn’t wait to take on the giants of cloud. And that still wasn’t good enough. They then jumped into the low margin grocer business.

Now, Amazon wants to take on Google and Facebook in mobile ads because they’re simply not juggling enough balls.

Rather than think about how Amazon can develop competitive advantages in the markets they enter, most investors see this and jump for joy. One more thing to boost the growth of the Everything Store, they say.

It’s why Amazon can continue to trade at a PE of almost 87. The momentum just hasn’t worn off yet. They keep tacking on new ventures, and this justifies the ridiculous growth assumptions investors have in their minds.

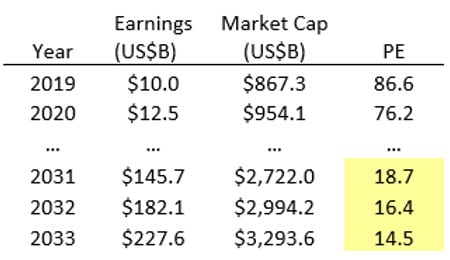

Even if earnings were to grow at 25% annually and Amazon’s share price was increasing by 10% per year, it’d take 12 years for the stock to reach a reasonable price compared to earnings…

Source: Money Morning

Does this seem achievable? Earnings growth of 25% for 12 years and a market cap of almost US$3 trillion in that same time…

‘But who cares,’ the people who’ve made money on Amazon say, ‘the stock keeps rising and I’m making money on it.’ Same goes for almost all of the top 10 fundie picks above.

But what happens when momentum fizzles out? What happens when our debt-filled system cannot limp along any longer? What happens when central bankers can’t continue to create easy money? And what happens when sentiment and confidence for ‘growth stocks’ shifts?

I think you have a pretty good idea what happens…like a game of Jenga, it all comes tumbling down sooner or later.

This momentum game is also why most funds do terribly. Most don’t beat the market. And most don’t survive in the long run.

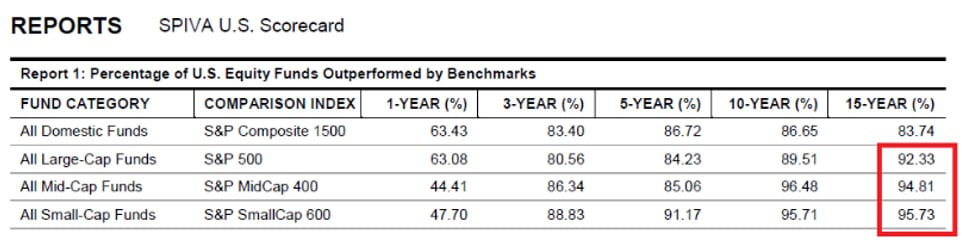

Source: AEI

The table above shows just how defeatist trying to beat ‘the market’ really is. Especially if you have a lot of money to put to work.

Over a one-year period, more than half (63.08%) of all large-cap funds can’t beat the S&P 500. More than 80% can’t do it over the next three years. And forget about the next 15…almost all large-cap funds do worse than ‘the average’.

But don’t disappear, dear reader. Things are not as dire for you as they are for most others…

Your secret weapon

Yes, you have a secret weapon. It’s you’re size.

You can head into places of the market where the ‘experts’ can’t follow. You can be one of 10 rather than one of a 1,000 who actually understands the stocks and their value down at the bottom of the market.

The experts have yet to gobble up many of these small-cap gems. And so, you have the opportunity to buy small potential beauties for cheap.

You don’t have to play the momentum game. You don’t have to pile into names like Amazon. There are plenty of opportunities down here in the small end of the ASX and NZX. And you’d be surprised by the kind of money you could make on some of these stocks.

All you’ve got to do is look…

Your friend,

Harje Ronngard

Harje Ronngard is one of the editors at Money Morning New Zealand. With an academic background in finance and investments, Harje knows how difficult investing is. He has worked with a range of assets classes, from futures to equities. But he’s found his niche in equity valuation. There are two questions Harje likes to ask of any investment. What is it worth? And how much does it cost? These two questions alone open up a world of investment opportunities which Harje shares with Money Morning New Zealand readers.