There’s a real sense of buzz at BizDojo Techapuna (Takapuna). Entrepreneurs doing stirring things. Talk of the next fundraising rounds. And those iconic views of the sparkling Waitemata.

I’ve come to have coffee with Rob Hanks. He’s managing partner with Curiat, Augmented Reality (AR) consultants. And he’s very excited about an AR future.

‘It’s going to be the Fourth Industrial Revolution,’ he says, mentioning a Goldman Sachs study that shows AR and VR (virtual reality) adding some $130 billion to world GDP by 2025.

So this emerging tech is about to generate revenue equal to over half of NZ’s GDP. Something for investors?

Rob Hanks is taking me through his presentation when we need to leave the theatre. A yoga class is about to start. And I’m wondering whether investing in AR is a bit of a stretch.

Now, most uses of AR that seem to add real value are in architecture, education, and in production processes. He mentions a large architecture firm bringing fit-out plans to life via wearable augmented reality. Clients can walk around their proposed new spaces.

It doesn’t seem market investable. Where’s the money?

Then Rob says something which changes the game. The real return on investment can be seen with high-value consumer brands, where there is a low-risk, repeatable purchase, and an experience can be added.

Consumer brands growing earnings with new innovations

As an investor, those are the sort of businesses I look for.

I find myself thinking of A2 Milk [NZX:ATM]. If you had invested just five years ago, you’d have multiplied your money around 14x.

The company rallied by $1 billion this week after a sharp lift in first-half profit. Extra nice was the lift in margins — up around 5% since last year.

Although the science is still evolving, milk with A2 proteins (as opposed to A1) is meant to make milk more digestible and comfortable, especially for people with lactose intolerance. It’s hot in China, where milk consumption is on the rise.

And A2 has found a way to charge a lot more for milk, which creates massive business value.

However, it looks to me a lot of A2’s growth may have already been had. The share looks expensive. And if the growth falters or the story starts souring, it could go the way of the Auckland property market. In other words, uncertain after a stellar run.

Plus, I’ve been involved in such businesses before. A big health story. Great margins for years. Then the tide turns with competition, market doubt and ‘nothing new’.

Augmented Reality can add growth to consumer brands

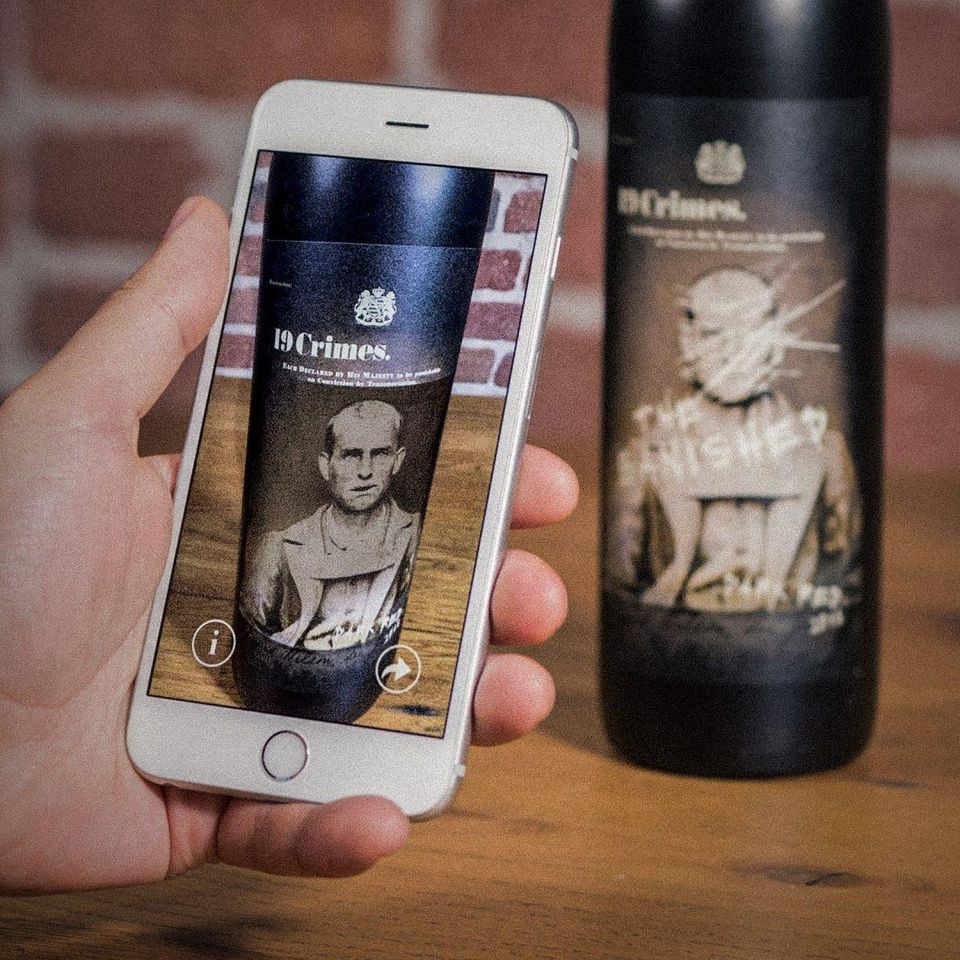

Rob Hanks shares with me his case study of the 19 Crimes brand of wines put out by Treasury Wine Estate [ASX:TWE].

Sales of Aussie wines have been in decline in the US for years. Then Treasury Wine put out AR-enabled 19 Crimes.

|

Source: Forbes |

Get the app, run it over the label and experience the historical story of one of the 19 Aussie outlaws displayed. And you can collect the ‘crime corks’, which lists the demeanours that got them shipped to Australia in the first place.

AR goes beyond a marketing gimmick to create an experience that drives earnings. [openx slug=inpost]

19 Crimes targets the crucial demographic of Millennial Men. Guys who like to identify with renegades. Start them appreciating wine early and you’ll have long-lasting customers coming to your brand.

Thanks to this innovation, Treasury Wine has shipped over a million cases, grown brand volume by 60% in sales and 70% in value.

Now, I’ve been looking for a wine company to invest in for some time. Not only because I enjoy a glass but because it’s a repeatable-purchase consumer brand. And I’ve spent some time analysing Treasury Wine and Delegat Group [NZX:DGL]. Delegat got away, doubling in value over the past five years while paying a small dividend.

Treasury Wine has done similar. However, like A2 Milk, it’s looking expensive right now (although not as expensive as A2). It pays a small dividend (2.3%). It’s enjoyed blistering earnings growth over the past several years that is now threatening to slow.

Having come off highs of $20 in late 2018, there could be the opportunity for steady and lasting performance. It’s still expensive, but with Australian market turbulence, a buy at around $12 could be appealing.

The bright spot is the marketing nemesis Treasury has shown with 19 Crimes and the willingness to embrace AR technology where it is well suited.

Should they continue to carve out leadership in this space, particularly in the growing US market and emerging Chinese one, I see continued and potentially dramatic upside for this company.

Lessons with consumer brands and AR

Experience tells me you need to exercise great caution and forethought when it comes to investing in consumer brands.

A few years back I followed Warren Buffett into Kraft Heinz [NYSE:KHC] (owners of our local Watties brand).

Kraft crashed 28% last week. The only upside has been the years of healthy dividend.

They were one of the first consumer-brand users of AR. In 2011, they trialled an app where you could unlock a pop-out recipe book when running your phone over a bottle of Heinz Tomato Sauce.

Kraft’s story is one of declining legacy brands, squeezed margins, and the inability to innovate fast enough to catch up with a changing market. Earnings are suffering as consumers move from packaged foods to organic, fresh, niche, and other food trends. And you don’t hear about them using AR anymore.

Kraft looks like GM did some years back. It needs fresh impetus.

Buffett’s statements on last week’s price fall are telling.

‘I have absolutely no intention of selling. I’ve got absolutely no intention of buying.’

He seems to think Kraft is still a ‘wonderful business’.

Now, Kraft is cheap. As GM has embraced EVs and self-drive, perhaps Kraft is in a similar position — it’s well-capitalised enough to embrace emerging food trends, AR, and the sort of high-growth-focused investments that can lead to tomorrow’s earnings rescue.

One thing’s for sure — the world is changing fast. I agree with Rob Hanks from Curiat: the next big thing will be some sort of spatial revolution changing our reality.

Success and profit will come from brands and businesses that can harness that power — and will go to those investors who can pick them.

Regards,

Simon Angelo

Editor, Money Morning New Zealand

Important disclosures

Simon Angelo owns shares in Kraft Heinz Company [NYSE:KHC] and General Motors Company [NYSE:GM] (via wealth manager Vistafolio).

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.