Editor’s Note: The Bonner & Partners offices are closed today for the Thanksgiving holiday weekend. In lieu of our regularly scheduled Diary, we share the below guest essay from Bill’s righthand man, Dan Denning.

As Bill reported last week, central banks are toying with the idea of launching a bank-backed cryptocurrency. Dan believes that outcome is all but assured. Only one thing stands in the way…bitcoin.

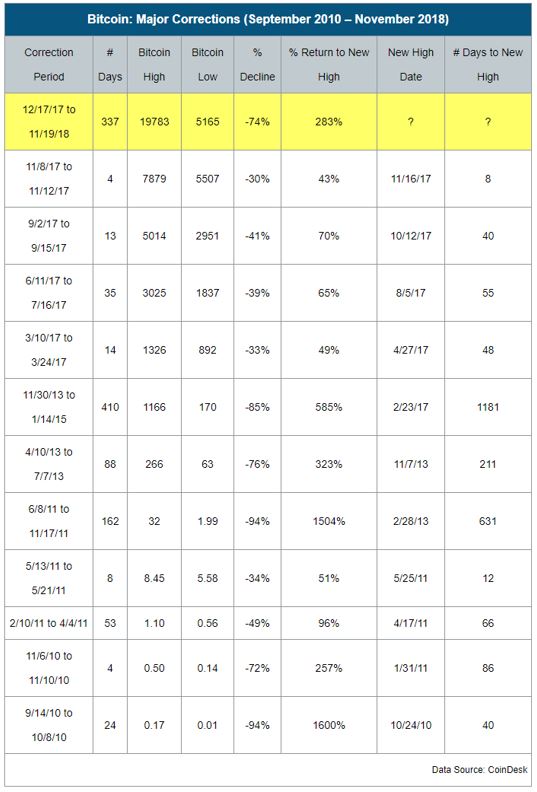

The collapse of bitcoin — down 68% year to date and 78% from its all-time high of $20,000, set in December 2017, when it traded at $4,200.22 earlier this week — may have a perfectly normal explanation.

It’s a bubble that popped. Or it’s happened before and is nothing to worry about. As my colleagues have shown their readers in the last week, bitcoin dropped 94% in 2010, 94% in 2011, 85% from 2013 to 2015, and 76% in a three-month period alone in 2013.

Big price declines are great buying opportunities, according to the bull case. In bitcoin’s case, any time the issue of a ‘hard fork’ comes up — where a blockchain has two paths forward and goes in both directions at once — you’ve seen big price declines.

But bitcoin has regrouped and rallied after each previous decline. It may do so this time as well. It may even be doing it as we speak.

Each of the previous rallies from a crash low came as the public became more aware of bitcoin. Awareness leads to liquidity and higher prices. This time around, for example, institutional interest in cryptocurrencies could be the catalyst for bitcoin to double from here (and then double again and again, if some of the crypto evangelists are right).

Crashes and corrections are normal for cryptos, right?

|

Data Source: Coindesk |

I’ll leave the technical discussions to some of my colleagues who are more qualified to talk about them. They’re important to understand if you’re a long-term holder (HOLDR) of cryptocurrencies.

Today, I’d like to suggest another explanation for the crypto swoon: the assassination of bitcoin by global financial authorities.

Why?

Cryptocurrencies have proven that there is an appetite for both a cashless digital payment system and digital assets. What central bankers and the world’s financial elite have figured out is that bitcoin stands in the way of this new world financial order.

It’s an order where centrally controlled digital money promises complete political power over the lives and choices of billions of people. They’re making their move to establish that order now.

Crypto is the evil spawn of the global financial crisis

A coordinated assault on cryptos took place over three days last week. Over those three days, from November 13 to 15, bitcoin broke through resistance at $6,330, fell to $5,508, and then, just kept on falling.

What happened? And in a moment, what happens next?

The Seven Deadly Paradoxes of Cryptocurrency: The first broadside fired at bitcoin came from the Bank of England’s blog, Bank Underground. Bitcoin is plagued by no less than seven fatal flaws, according to John Lewis of the Bank of England’s research hub.

Among these flaws is the fact that 97% of bitcoins are held by less than 4% of addresses, creating a hoarding mentality that limits the liquidity of bitcoin and its popularity as a payment option.

Another: Bitcoin can only process seven transactions per second. Visa does 24,000 per second.

Another: Innovators who build on the foundation laid by bitcoin will, by definition, improve and replace it. Its obsolescence and eventual destruction are the inevitable consequence of its conceptual success.

The Case for a New Digital Currency: Central banks should create digital currencies and play a critical role in the global payments system, including the settlement of transactions, argued International Monetary Fund president Christine Lagarde in Singapore on November 14. It was a subtle argument in its focus on potential public/private partnerships between commercial banks and central banks.

But the important point is that Lagarde publicly floated the idea that central banks — not the private sector — should create and manage digital currencies. Centralisation allows for control. Decentralisation does not.

Evil Spawn: Bitcoin was a clever idea, but not a terribly good one. Worse, it was the ‘evil spawn’ of the financial crisis of 2009, according to Benoȋt Cœuré from the European Central Bank (ECB). Cœuré quoted Agustín Carstens, general manager of the Bank for International Settlements, who called bitcoin ‘a combination of a bubble, a Ponzi scheme, and an environmental disaster.’ Cœuré’s speech called for further research into a central bank digital currency, but concluded it could be at least a decade away.

Why the three-pronged full-frontal assault on bitcoin right now? Because it’s a threat? Because it’s vulnerable to a lack of public trust? Or because now is a perfect opportunity?

It’s a combination of all three. But the last more than the first two. True, bitcoin was a response to the financial crash of 2009. It was a perfectly rational response to a system run by financial elites that holds your money captive, systematically destroys the purchasing power of your savings, and creates wealth-destroying booms and busts that are increasingly politically and socially destabilising.

What fool wouldn’t want to get their money out of a system like that?

To the extent that cryptos could create a decentralised payment system/currency/asset class where trust is guaranteed by the blockchain, it’s a kind of sound-money, libertarian nirvana.

But the flip side is that the moment that decentralised system becomes an actual threat to the money system controlled by central banks, the full might and power of sovereign states and central banks would come down on it. That’s what’s beginning to happen now.

Is bitcoin vulnerable to a lack of public trust? Vast swathes of the public still don’t know about or understand bitcoin. The interest it has attracted in the last year is largely speculative. It’s not people betting on a new, disruptive technology or money system. It’s people trying to make a quick buck from higher prices. And by the way, you still have to sell back into a fiat currency to make that buck, yen, pound, or euro.

That leaves the last possibility. Last week’s attack on decentralised cryptocurrencies comes when the price action is bearish anyway. It also comes as central banks are ready to advance all the benefits of a central bank digital currency. Central banks aim to capitalise on the budding popularity of cryptos and then harness it for their own ends. So what are their own ends?

The war for control of digital money

The financial elite took its attack on cryptos to the front pages of the paper this week. Economist Nouriel Roubini argued in The Guardian for a central bank digital currency that replaces the current payments system and the money creation function of commercial banking (although not the lending, which would be fully funded from 100% reserves).

In Roubini’s version of a central bank digital currency (CBDC), there’s no blockchain technology at all (it’s not scalable, cheap, or secure, he argues). And in his version, decentralisation is to be avoided. Centralisation is a desired (and necessary) feature for monetary control.

There’s just one problem: What role do the banks play? You know, the banks that run Wall Street and control the Federal Reserve System. According to Roubini (emphasis added is mine):

‘The main problem with CBDCs is that they would disrupt the current fractional-reserve system through which commercial banks create money by lending out more than they hold in liquid deposits. Banks need deposits in order to make loans and investment decisions. If all private bank deposits were to be moved into CBDCs, then traditional banks would need to become “loanable funds intermediaries,” borrowing long-term funds to finance long-term loans such as mortgages.

‘In other words, the fractional-reserve banking system would be replaced by a narrow-banking system administered mostly by the central bank. That would amount to a financial revolution — and one that would yield many benefits. Central banks would be in a much better position to control credit bubbles, stop bank runs, prevent maturity mismatches, and regulate risky credit/lending decisions by private banks.’

It’s all about control. Cryptos and bitcoin threaten that control. They have to go. Bitcoin gets knifed in the back by the IMF/SEC/NSA and we get a digital money system where cash disappears and the authorities have full transparency into our monetary affairs. Our worst nightmare, in other words.

A forked road

We’ve come to a fork in the road for the money system (since we were talking about forks). The traditional Wall Street money power controls the system because it’s the quickest means to vast wealth (as Bill has shown in the Diary the last few weeks).

Control over money is sought for the purpose of wealth. The power of banks to create money is important, but incidental to the goal, which is filthy lucre.

But the centralising, authoritarian, statist monsters, though, seek control of money because their real goal is political power. This is the War on Cash that Bill and others have written about for years. It is the systematic destruction of your ability to collect and hold wealth outside of the financial system.

Killing the direct convertibility of the US dollar to gold was one step. The various laws and regulations, like civil asset forfeiture, which allow authorities to seize ‘suspiciously large’ amounts of cash without due process, is another. The assassination of bitcoin will be the next.

It just so happens that the money system, with the advent of technology and a cashless society, is now the fastest, cheapest, and most thorough route to complete political power over the lives and private choices of billions of people.

Fractional-reserve banking is a time-tested strategy for controlling money for the purposes of the acquisition and growth of large personal fortunes.

But the issuance of a central bank-backed coin is an emergent claim that the power over money should be centralised to nudge/control/coerce the population for its own moral betterment.

The Wall Street crowd could get completely blindsided by the DC crowd in the digital money war. Either way, ordinary Americans may be caught in the crossfire. The time to protect yourself is now.

Regards,

Dan Denning

Co-author, The Bill Bonner Letter

PS: If history has shown us anything, it’s that centralised authorities will do anything to maintain control over money. Does bitcoin pose a threat to that control? I believe it does. But the assassination of bitcoin will be just the first step…

Dan Denning examines the geopolitical and economic events that can affect your investments domestically. He raises the questions you need to answer, in order to survive financially in these turbulent times.