Corrections.

Crashes.

Ouch.

Is just thinking about it enough to make your stomach lurch and give you sweaty palms?

Well, you’re certainly not alone. Many investors feel exactly the same way you do. Anxiety over ‘what if’.

Source: The McDowell News

Yet here’s an undeniable fact: the next shock event is almost certainly coming.

Yes, sir. Guaranteed. Absolutely.

Here’s what it looks like:

- A correction happens when the market falls 10% or more from its recent high. This decline can unfold over days, weeks, months.

- A crash is more sudden and much sharper. It’s a deep dive of 10% or more in a single day.

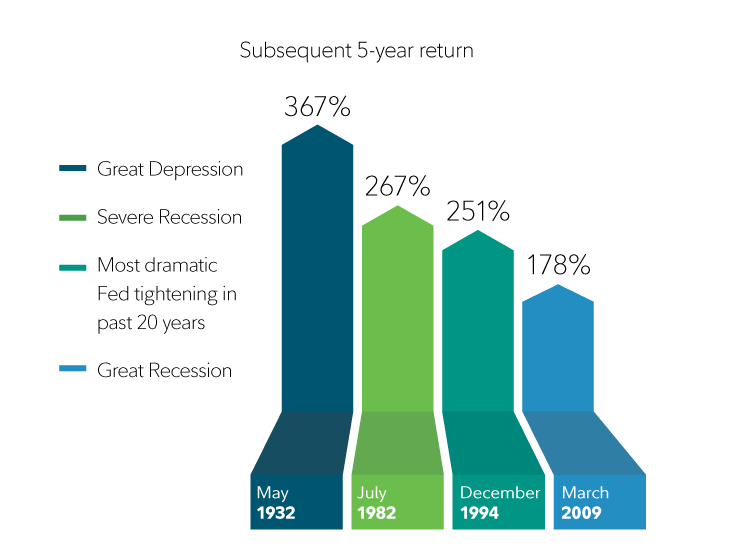

While it’s impossible to predict with certainty when the next correction or crash will happen, we do have a wealth of historical data.

Here’s what the past tells us:

- Corrections are pretty common.

- Since World War II, the S&P 500 Index has experienced 28 corrections.

- On average, this works out to be a correction roughly once every 2 years.

- The average decline each time is around 14%.

Timing the market?

So, given the facts, some of you might be wondering:

- ‘Why don’t I just hold on to all my cash?’

- ‘Why don’t I wait until a crash actually happens?’

- ‘Why don’t I deploy my money then?’

Aha. These are very good questions.

Peter Lynch, the legendary fund manager of Fidelity Magellan, has a witty reply for you:

‘Far more money has been lost by investors preparing for corrections than has been lost in corrections themselves.’

Source: Fidelity

Here’s the issue. We human beings are terrible at timing the market. And when we do try, we almost always lose money.

- For example, it may feel logical for us to try and avoid the pain of a correction by staying out of the market entirely.

- However, this becomes a self-fulfilling prophecy, where we actually inflict more financial pain on ourselves over the long-run.

- Over a 40-year hypothetical period, just missing the best 10 days of our investment journey cuts our income by nearly half.

- Missing the best 50 days is even more disastrous. Our income shrinks by over 90%.

So, you have to ask yourself honestly: is your fear of a correction a good enough reason to stay out of the market? Especially when the upside could be more positive than you believe?

Source: Fidelity

Invest for long-term value

At the time of writing, the annual rate of inflation in New Zealand sits at 6.9%. It’s anyone’s guess what it will look like by the end of the year.

None of us have a crystal ball. But this much is clear: life is about managing risk. And there is a clear and present danger right now of seeing the value of your cash fade due to inflation.

Your opportunity cost is what you could do with your funds instead.

Could you be earning dividend income? Along with some capital growth? Without having to buy into New Zealand’s expensive property bubble?

Given this inflationary environment, simply waiting and doing nothing may be the biggest risk of all.

Protecting wealth. Growing wealth. It’s never been more urgent to do so.

Do you feel the same way? Would you like to talk to us?

We are now offering free consults for Eligible and Wholesale Investors.

Rest assured, we’re always here for you.

Rain or shine, boom or bust, we can help you put together the ideal plan for the rest of your financial journey.

Regards,

John Ling

Analyst, Wealth Morning

(This article is general in nature and should not be construed as any financial or investment advice. To obtain guidance for your specific situation, please seek independent financial advice.)