Westpac Banking Corporation [ASX:WBC] [NZX:WBC] saw its share price fall around 6.5% today.

Westpac is Australia’s oldest bank. It has about a 21% market share of mortgage lending in Australia, and 18% in New Zealand. It typically does well from the margin on this lending.

The fall today was a surprise. The price had been rising following economic recovery from the pandemic. Results announced today showed the net profit up over 138%, a solid dividend, and further return to shareholders via a buyback.

But it wasn’t enough for the market, given previous analyst expectations.

Let’s take a look at what’s happened. And whether this dip could provide upside on Westpac today.

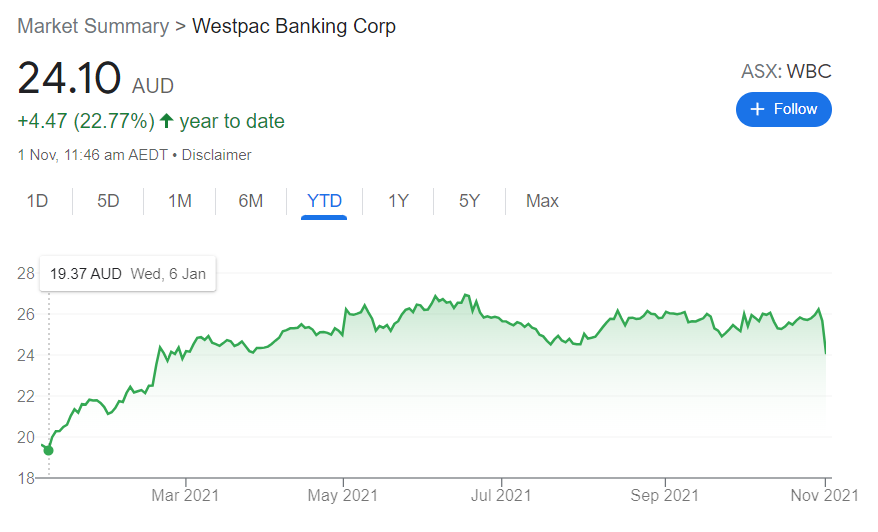

Why has the Westpac share price fallen?

Source: Google Finance

For a start, Westpac has had a rapid ascent since the start of the year, growing some 23%.

This is slightly higher than ANZ, which grew 20% over the same period. The dividend yields for both banks are very similar.

The FY21 results announced today were much anticipated. But they didn’t meet ambitious recovery expectations by analysts:

- Statutory net profit up 138% to A$5.46 billion.

- Cash earnings up 105% to $5.35 billion. (Analyst consensus was $5.42b).

- Higher final dividend declared at 60c per share (118c for the year).

- Announced $3.5 billion off-market share buyback. (Analysts expected $4-5 billion).

- Net interest margin (NIM) down 4 basis points to 2.04%.

Where could Westpac go from here?

Lower-than-expected earnings have stemmed from that critical net interest margin, which is down.

Yet net interest margins in Australasia are still much higher than we see with another large bank we follow in the UK. For example, in Britain, these have been in the range of 1.07% to 1.33% over a similar period.

Earnings are only 1.3% off consensus expectations. A sell-off causing a 6%+ drop seems a little heavy. Though the option for existing shareholders to sell into the buyback at a discount of 8% to 14% also adds pressure.

In this environment, where markets are high again, it is the ongoing dividend income that interests me. The gross yield looks to be around 5% p.a. Likely far better than any term deposit the bank itself could offer you right now.

Now, with inflation and higher interest rates on the cards, I also expect that net interest margin could even lift a little in the short to medium-term. There could be upside.

But there’s also risk. If the inflation is persistent and impacts the housing market, this could lead to wider risks for the banking sector.

The results announced today look solid for long-term investors considering the past year. The dip on missed expectations potentially presents an opportunity. Yet there are storm clouds on the horizon.

Some interest rate rises may be positive for banking — but a more sustained downturn in critical mortgage markets could be destructive.

Regards,

Simon Angelo

Editor, Wealth Morning

(This article is commentary and the author’s personal opinion only. It is general in nature and should not be construed as any financial or investment advice. To obtain guidance for your specific situation, please consult a licensed Financial Advice Provider.)

Important disclosures

Simon Angelo owns shares in Westpac [ASX:WBC] via portfolio manager Vistafolio.