Eroad Ltd is a transport technology-and-services company based in New Zealand.

It provides an innovative electronic solution to manage and pay road user charges (RUC). It also supports regulatory compliance and provides commercial services to the heavy-vehicle industry.

Source: Eroad

In 2009, Eroad [NZX.ERD] revolutionized RUC and regulatory compliance by offering the world’s first GPS/cellular-based tracking-and-charging system.

This innovation has now been wholly implemented in the New Zealand market, superseding the paper-based process before it.

Eroad’s variety of product offerings continue to dramatically reduce the amount of time and money spent on RUC compliance. They also provide accurate data and fleet management for clients.

Following the success that Eroad has had in New Zealand, the company subsequently expanded to North America, launching operations in Oregon. Eroad also listed on the ASX in 2020.

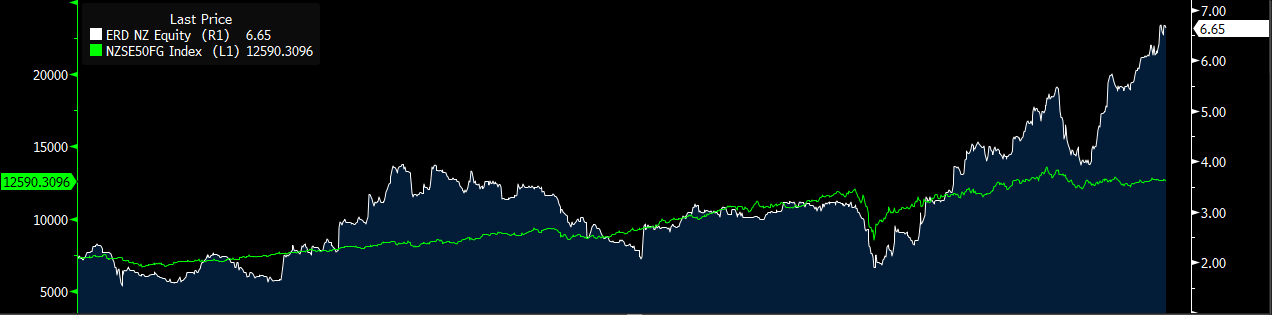

The graph below illustrates [NZX.ERD] stock returns over the last five years (highlighted in white), compared to the NZX 50 Index (highlighted in green).

Source: Bloomberg LP

Financials and performance

- According to the Eroad full-year report, released 28th May 2021, revenue grew to $91.6 million. This constitutes a 13% lift from FY20.

- The New Zealand segment generated $59.8 million of this revenue.

- The American segment generated $30.6 million.

- The Australian segment generated a modest $1.4 million.

- Subsequently, EBITDA also rose by 13% over the same period.

Eroad’s ability to consistently improve on past performance can be credited to their accelerated growth strategies and clientele management.

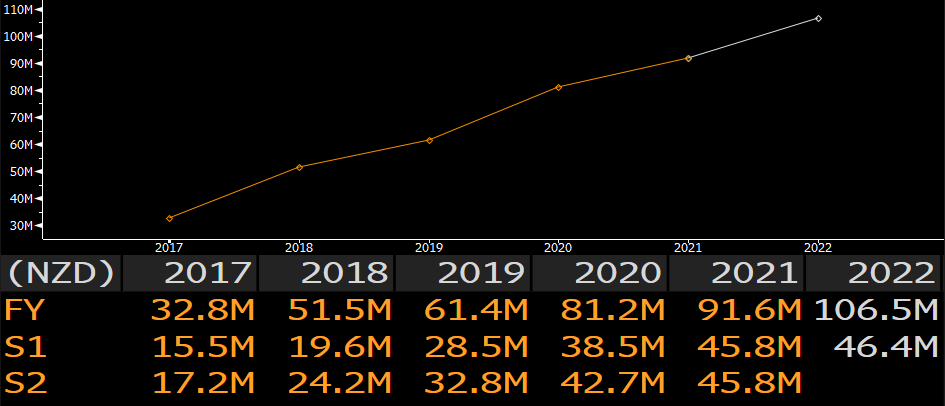

The graph below highlights [NZX.ERD] revenue figures over the last four years.

- We can see a clear trend of growth ever since 2017.

- The grey figures under 2022 are analyst estimates by Bloomberg LP.

- The consensus estimates the trend to continue, which is positive for investors.

Source: Bloomberg LP

Consistent revenue growth is certainly a good sign when looking at the overall competency of a company. It adds confidence to the perceived value of the product offering.

But here’s the big question: ‘Is this growth sustainable?’

Remember: Past performance is never a guarantee of the future.

In my opinion, I believe that as long as [NZX.ERD] continues to play its cards right, it may continue to take advantage of immense expansion possibilities, domestically and globally.

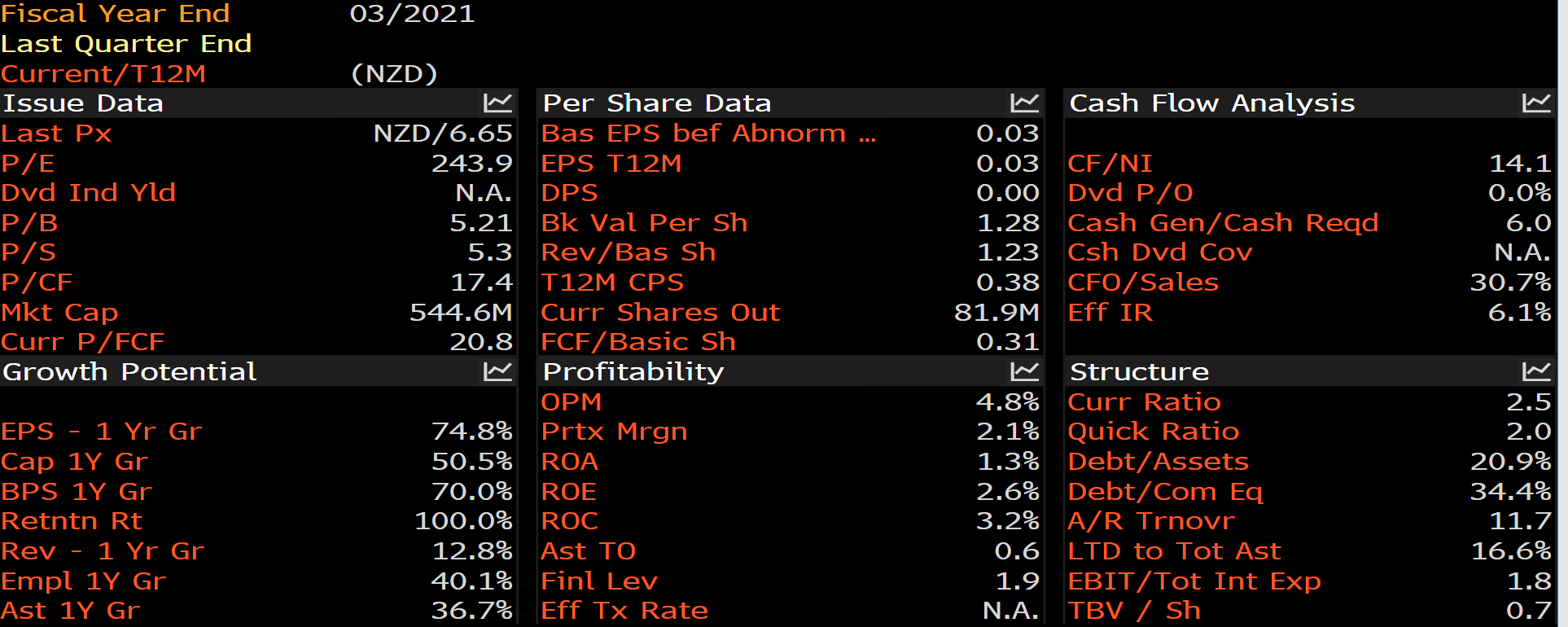

Source: Bloomberg LP

Presently, a deeper analysis is crucial in gaining a better understanding of the underlying financial health of the company.

In the case of [NZX:ERD], the first thing any analyst would get wide-eyed at is its P/E.

- The price-to-earnings ratio measures the current share price of a company relative to its earnings.

- It’s used in stock valuation to determine whether a stock is overvalued or undervalued.

- The average P/E ratio for the New Zealand over the past decade has been around 15.

- Eroad’s current P/E ratio is 243.9, which looks exceedingly high.

Does this mean that [NZX.ERD] is overvalued?

Here are few points to consider:

- Growth stocks in the technology sector generally tend to have a larger price-to-earnings ratio.

- It may mean that the market is willing to pay a higher price due to positive sentiment around the stock’s future growth prospects.

- In all likelihood, it might be safe to assume that future earnings have already been factored into the current share price for [NZX.ERD].

Another possible indicator of future growth that we can deduce from this data is the retention rate.

- Eroad’s 100% retention rate is impressive.

- It means that every single dollar of earnings is retained and reinvested back into the business in order to fund future growth.

- This means, however, that the company is not currently paying any dividends to shareholders.

There’s also final point I want to touch on, which is the current ratio and quick ratio.

- These ratios define the company’s ability to pay off its short-term obligations with its liquid assets.

- Its current ratio of 2.5 indicates that they would be able to pay off their liabilities 2.5 times with their current assets.

- This seems to suggest a measure of sustainability for the company, especially if it needs to pay down debt in the worst-case scenario.

Coretex acquisition

What does the immediate future for Eroad look like?

Well, a unique opportunity appears to be on the cards.

Eroad has recently entered into a conditional agreement to acquire 100% of Coretex Limited for approximately $158 million.

- Coretex Limited was initially a competitor to Eroad, also operating out of Auckland, New Zealand.

- The acquisition has been expected to complete in the second half of 2022, but it is subject to conditions.

- According to Eroad CEO Steven Newman, the current shareholders have placed their utmost confidence and support in the decision.

Newman states that while the two companies operate in the same countries, they have different strategies. By coming together, they will be poised to continue expansion and gain a greater share of the global-vehicle telematics market.

It’s a market that’s estimated to grow to $750 billion by 2030.

Covid-19

There’s no hiding it: The pandemic remains a threat. Many businesses have been seriously affected by the lockdowns in 2020 and 2021.

Fortunately, Eroad was one of the lucky ones.

Steven Newman said that the company has overcome these challenges to embrace fresh opportunities. Following New Zealand and America’s rebound from the pandemic, Eroad is now stronger than ever. The company is set to position itself for increasing growth.

It is reassuring for the prospective investor to note that [NZX.ERD] had a fantastic Covid response. Even through the toughest period, the company has managed to improve its profitability. This is really a showcase for excellent managerial skills and flexibility in uncertain times.

Key risks

- Competitor Risk

Although Eroad has optimised its products for success, competition is looming from American services such as Verizon Connect. Eroad will need to keep innovating to stay ahead of the curve.

- Customer Retention

Eroad needs to ensure that it has a strong enough moat. This is inherently critical to its revenue and success. So far, it has done this successfully. The [NZX.ERD] customer retention rate is very high at 95%.

- Failure to Execute Merger/Acquisition

The acquisition of Coretex Limited will cost a hefty sum, but it is expected to improve Eroad’s contact-and-supply network. However, if the merger fails to go ahead, it could have a drastic impact on Eroad’s future prospects. Shareholder confidence could fall drastically.

- Foreign Exchange Risk

A third of the company’s revenue comes from America. This figure may continue to grow in the future. But it’s important to be mindful that the exchange rates between currencies may have an effect on company earnings when reporting in NZD.

Conclusion

Overall, Eroad seems to be a stable company with great management and sound growth prospects.

We can assume that it will continue to innovate and invest in itself as it continues to increase its market share in this growing industry. But be aware: Past performance is never a guarantee of future performance.

It is always difficult to tell whether now is the time to buy, especially as Eroad has only just offered a discounted share purchase plan to eligible shareholders this month.

Some may find the current price too expensive at the moment. I wouldn’t be surprised if it has already hit its price ceiling.

The real question is this: ‘How much of the company’s future growth has already been factored into the current price?’

Regards,

Samael Knaap

Analyst, Wealth Morning

(This article is commentary and the author’s personal opinion only. It is general in nature and should not be construed as any financial or investment advice. To obtain guidance for your specific situation, please consult a licensed Financial Advice Provider.)