Wealth looks for a safe harbour. Where it won’t get eroded. Taxed. Squandered by hangers-on. Or decline in illusory markets subject to shock.

It’s 2017. I’m visiting a family office in Jersey, Channel Islands to discuss investments. There’s an odd juxtaposition. A swanky new glass building overlooking the bay at St Helier. Filled with old mahogany sideboards and cabinets. Century-old antiques.

Protecting family wealth — the business of a family office.

Source: Heavens LLC

The guy I’m meeting picks up on my glance. ‘They’re all from the old ships,’ he says. ‘This family made their initial fortune in the shipping industry in the 1800s. Today they’re in property, public stocks…’

And so the conversation goes.

Family offices and trusts in stable, tax-neutral jurisdictions like Jersey are controversial. In nearby England, the assets could be liable for inheritance tax. In France, you get this and wealth tax too.

Such trusts often allow for income to descendants. But not the capital, which is preserved for generations to come.

Lessons of wealth and succession-planning are golden

Here in New Zealand in 2020, we’re seeing two interesting phenomena:

- An increase in wealth of global scale due to the rapid escalation of real estate prices.

- A large influx of money as newly minted millionaires, especially from Asia, look to find a safe haven and capital-gains-free home for their wealth. Along with a more relaxed lifestyle.

A similar trend is at play in Australia, though there is a limited capital-gains tax there.

Unlike the old European shipping fortune, built on productive pursuit, then invested in global assets, wealth in New Zealand is increasingly concentrated in just one area.

Real estate.

Investors associate the New Zealand economy with dairy and tourism. Another significant wealth area is housing. Buying and selling to each other. Selling to wealth-refuge migrants. And then renting to a massive property underclass unable to keep up with runaway prices.

It is unlikely any political party will disrupt the gravy train. There are too many mum-and-dad investors sitting in first class. But market forces could put a kink in the tracks.

Unsustainable solution for housing

Look at the extent housing plays in the Australasian economies:

| Country | Housing market (total value) approx. | % of total household wealth approx. | Ratio to national GDP | Ratio to stock market value |

| New Zealand | $1.13 trillion | 72% | 3.9x | 7.2x |

| Australia | $6.6 trillion | 49% | 3.5x | 3.3x |

| United States | $33.3 trillion | 29% | 1.6x | 1.5x |

The housing market is not just housing in New Zealand. It’s investment. Property is now more than 7x the value of the investment in productive businesses on the stock market!

Protecting the wealth of this country comes down to protecting the value of property.

Now you can understand why the two major political parties, National and Labour, have a vested interest in maintaining very high rates of net migration.

But this is not a sustainable solution. There are two classes emerging.

- Those who have caught the property windfall over the past decade

- Those who have missed out completely

History tells us that such situations lead to crisis.

But it may take another decade or two for that to play out.

Meanwhile, people use ever higher levels of debt to enter the market. And that heightens the dependence on low interest rates.

At the moment, these rates look to be stable. But it would not take too much more than a major world crisis — watch the Middle East right now, a trade-recalibrated Chinese depression, or another natural disaster at home — to increase the risk premium on Australasian interest rates.

What can investors do to preserve wealth?

What the numbers show is this: while other very wealthy countries like the US have significant investment in housing, they also have more significant investment in financial assets.

Financial assets like shares tend to be more liquid, diversified, and global. They also tend to align more to real economic growth, such as an increase in GDP. Or a specific business or sector opportunity.

When you have a situation where capital is being mobilised predominantly into housing, financial markets get constrained.

The other issue is that there is a lack of good quality companies on the NZX.

Given the property shortage in New Zealand, you have to ask the question: why is there not a single, focused home builder listed on the NZX?

There are several in Australia. And there are many in the US and Europe, where lower income to property-value multiples are evident.

Again, capital here focuses on the potential gains in existing property. Not the development of much-needed new build and efficient scale.

To me, there appears clear reason to invest in stocks globally. To diversify and preserve wealth beyond housing into dynamic financial assets. And to take advantage of any comparative strength in NZD when it exists.

What can the government do about housing?

By almost any global comparison, housing in New Zealand is severely unaffordable. Many people, especially younger buyers, are taking on substantial debt. This is contributing to some of the highest household-debt ratios in the world.

In my search for sensible policy, I could only find only one party with a clear understanding of the economics.

Labour acknowledges there is a housing crisis and has dealt with foreign and local speculation. But so far, their published policies seem to have barely stemmed the tide.

National’s website seems to only have their 2017 promise to somehow build 200,000 homes. They want to pave the way with new infrastructure and first-home buyer grants and lending.

Neither political party seems to understand that structural supply won’t meet the demand of forced population growth. But they cannot forego the latter since they are focused on short-term growth as opposed to long-term wealth.

A conservative approach

In my search for a coordinated approach, the New Conservative Party has offered refreshing insight.

They have a total housing policy, covering supply and demand, while addressing the issues involved: costs, skills and regulation.

When questioned, leader Leighton Baker provided a clear view on the subject:

‘As a party we believe the ownership of New Zealand land should be restricted to Citizens and residents as this inhibits foreign speculators and keeps the non-renewable resource of land under New Zealand ownership.

‘We have been quite consistent in calling for net zero immigration to allow our housing stock to grow to meet current demand. Generally immigrants require significant capital to immigrate so they are able to get on the property ladder, this means those at the bottom of the ladder in New Zealand are simply pushed lower down.

‘The housing issues we face are nothing new. Do not require rocket science, but they do require a multifaceted approach in regards to availability, affordability and quality.’

This is correct. The housing crisis comes down to a demand-and-supply problem. Although yields are under pressure, there is speculative investor opportunity. Providing property demand continues to get fuelled by high migration and low interest rates.

Of course New Zealand needs quality migrants. But should first ensure the housing market works justly

The danger is that a shock to either of these forces — as opposed to a managed adjustment — could pull down the market and rock the economy.

Failing to address this will continue to inflate a tinder box of illusory wealth that investors should be wary of.

Where do the wealthiest investors put their money?

There have been fast rises in Asia and the developing world, but this trend is sometimes overcooked by the mainstream media. Many people in the developing world still live in abject poverty.

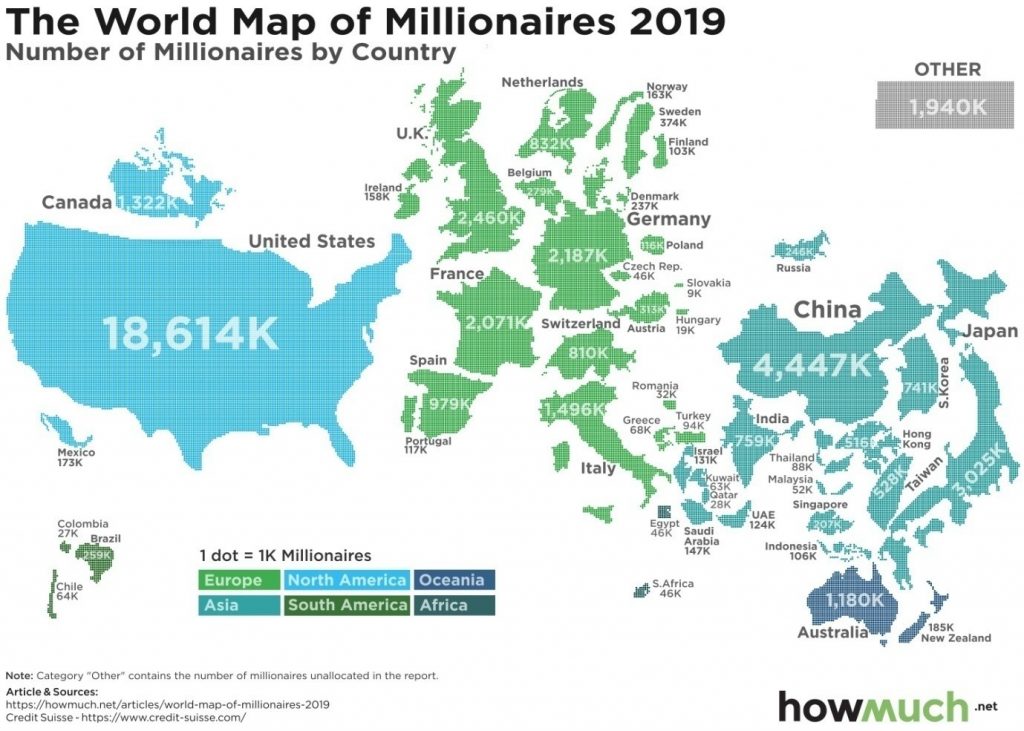

In 2019, the world’s wealthiest investors live primarily in one area of the globe. Some 71% of the world’s millionaires live in Europe and North America. The United States is the single largest home of wealth on a global scale:

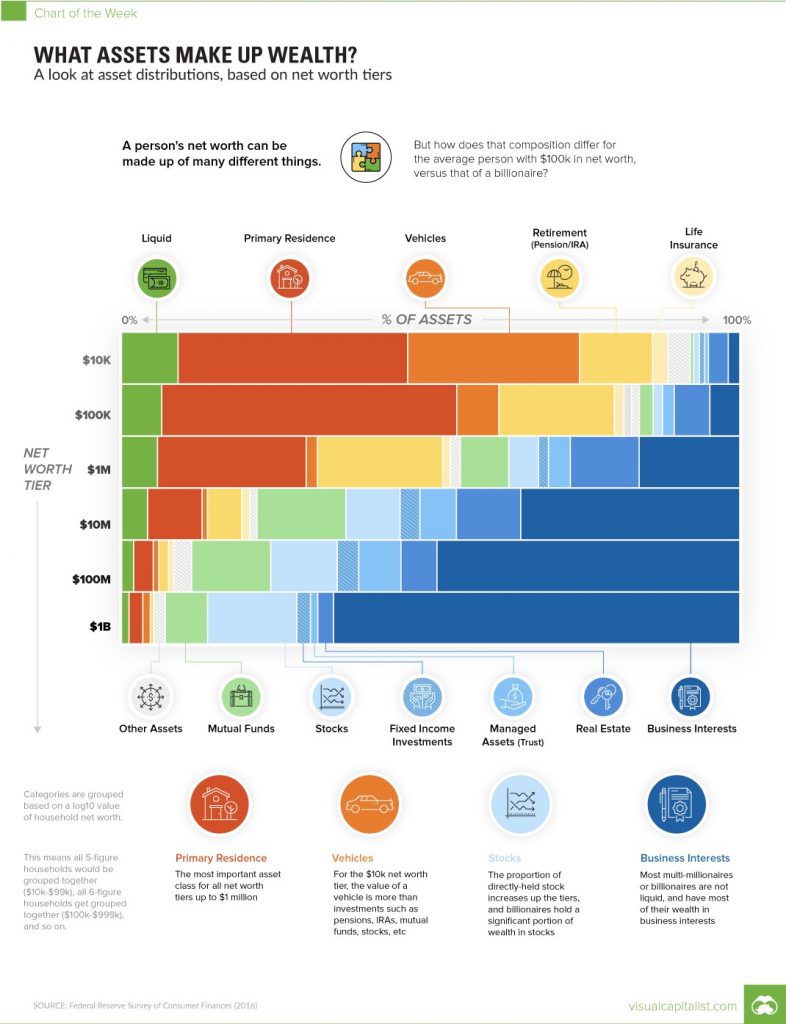

Now take a look at where Americans with a net worth of $1 million or more put their wealth:

The primary residence and real estate form less of a person’s net worth as they become wealthier. And they make up less than half of assets for millionaires.

So, at high levels of wealth, real estate becomes less of a source of wealth as compared to stocks, funds (financial assets) and business interests.

The point is that we could be over-invested in housing and real estate in New Zealand — and possibly Australia too.

For now, this may work as we attract significant migration from the developing world and borrow at historically very low interest rates.

I hope there will be a managed correction of the housing situation in New Zealand, as at least one measured political force has proposed.

If some sort of crisis does ensue, the blood flow could be unstoppable.

Meanwhile, there is justification to consider more diversified financial assets as a key part of investment planning.

Is your wealth invested in a safe harbour?

Regards,

Simon Angelo

Editor, Wealth Morning