More than a thousand 20-somethings came to see Captain Hoff in San Francisco.

They were there for the Founders Conference.

It’s a conference chock full of start-up founders.

Not all are successful. But they hope they will be, some day.

As part of the conference, Hoff plans to incubate 100 start-ups over five years. Of those, about half will receive Series A funding (first round of start-up funding).

It’s a chance of a lifetime for many young entrepreneurs.

What could be better than millions in funding and advice from the co-founder of LinkedIn, the professional social network?

This year, however, Captain Hoff was a tad more pessimistic than usual.

While waiting for guests to arrive, Hoff said he was going to hold onto a lot more of his money. What’s got Hoff concerned is the recent dip in tech stocks.

For the longest time, tech has had a dream run. Valuations soared. The private start-up scene rose to new heights.

But all that could come to an end. And Hoff is expecting it will.

He fears you’ll see more declines, not just for tech stocks but also private start-ups values.

It’s why he’s holding onto more of his US$1.7 billion than usual.

Should you do the same?

What is causing the market-wide crash?

You may have noticed, especially if you own one, that tech stocks are down again.

The NASDAQ is creeping back down to its lows of 2018.

Tech stocks on the ASX are following.

Stocks like Altium Ltd [ASX:ALU] and Afterpay Touch Group Ltd [ASX:APT] dropped more than 5–10% yesterday.

Even the tech-affiliated bitcoin is nose-diving.

The crypto now sits at US$4,285 — one of its lowest points this year.

And what’s causing all these declines?

Valuations. Interest rates. Growth assumptions.

There are a lot of reasons why fund managers don’t want to be in tech.

Yet recent selling has nothing to do with any of the above.

If valuation really dictates investment decisions, why were these stocks bid up just months ago?

Take Apple, Inc. [NASDAQ:AAPL].

Fundies now think the stock is too expensive. Apple trades at 15-times earnings. So why were they buying Apple months ago when it was trading at a much higher price?

The same goes for many other tech names.

Why all of a sudden have they changed their views on technology? If it was so obvious that these stocks are overvalued, or that interest rates would rise, why were they bought at much higher prices?

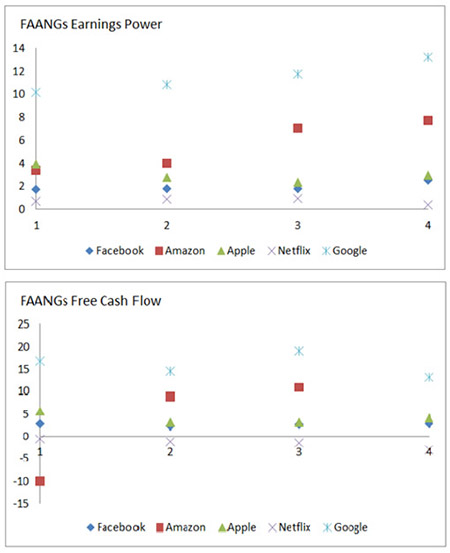

Are earnings dropping? Not really.

Take a look at the FAANGs. In the last four quarters of 2018 (some Q4 figures are estimates), earnings and free cash flow haven’t fallen off a cliff.

|

|

Source: Bloomberg |

Yet, these four tech stocks have been murdered from their highs this year.

|

|

Source: Bloomberg |

To me, it seems pretty obvious what’s going on.

Fundies think they can time the stock market

Fundies think they can time the market. And they’re using excuses like high PEs, rising interest rates, potential regulation and lagging growth to justify their actions.

I tell this to my father and he recoils.

How can this be possible? These are professional money managers, with decades of experience and education. They must be enormously smart. It’s why they’re paid so much money.

I cannot argue with the latter.

Most fundies are very smart. They know exactly the game they’re playing. If they underperform in the next 12 months, say goodbye to a whole lot of clients.

It’s why they feel they need to try and time the market.

If tech stocks are raging ahead and you don’t jump on that train, valuable or not, you fall behind the pack (in the short-term) and risk losing a whole lot of money.

Need more convincing?

Just take a look at what Lachlan MacGregor of Alphinity Investment Management wrote in June this year:

‘Technology has had a dream run over the last year, up 34% in the 12 months to last Friday and beating the index by 17%. Apple, Alphabet (Google), Amazon, Facebook and Microsoft accounted for almost 40% of the performance of the S&P 500 index year to date.

‘If you were underweight Technology, and in particular these mega-capitalisation FANG stocks, you probably underperformed the index. Banks, the winning sector in Q4 2016, [have] underperformed the market by 6% since the start of the year.

‘As a result investor positioning in Technology shares is at extreme levels with investors crowding into these winners. The sell-off on Friday was concentrated around the best performing, highly liquid mega-cap stocks as they were the easiest stocks to sell quickly. It is interesting that the selling on Wednesday and Thursday was more broadly based across the whole sector.’

Fund manager Jim Cramer said more or less the same thing in September. Fundies were trying to time their profits and jump onto the next rising sector.

‘This sell-off is all about the mechanics of the money management business. As I told you in Tuesday[’s] show, high-flying tech stocks tend to get hit in September as people try to take profits before someone else takes them for you.’

The market is there to serve not instruct

Of course, there’s nothing wrong with trying to time the market, even though it fails to outperform.

The problem I have is that many managers aren’t willing to admit this is what they’re doing: betting on when a sector will rise or fall.

The reason they don’t is because there so much academic evidence showing how terrible market timing can be.

I’m not telling you to buy the FAANGs, or even a majority of tech stocks right now. But I think you’ll find it helpful if you stop looking for reasons why stocks are rising or falling.

Many of the reasons tossed out by fundies and market commentators are just excuses. And they use them to justify why they’re jumped out of tech stocks.

It’s not because those stocks are falling and they will push the fund’s performance behind the average. It’s because of high PEs, rising bond yields and all that jazz.

Remember, the market is there to serve you, not instruct you.

Each day it throws prices at you. And you can decide whether to buy or sell.

Sometimes these prices are ridiculously low. And that’s when you’ve got to load up.

Most of the time however, you won’t know whether a price is low or high. It’ll be somewhere in the middle. And that’s when you’ve got to keep searching for undiscovered opportunities.

All you really need is a few good investments. In the extreme case (Captain Hoff’s case), all you might need is one.

Your friend,

Harje Ronngard