On Thursday, Facebook founder and CEO Mark Zuckerberg lost $17.7 billion in just 24 hours, after Facebook shares went into a nearly 20% freefall.

The market losses were estimated to be around $177 billion in total.

According to the NZ Herald, that was the ‘worst single-day evaporation of market value for any company’.

Oh the terror!…now Zuckerberg’s only worth $110 billion.

You’ve got to wonder…what went on in his head as the shares were dropping?

Was it fear? Stress? Anger?

He doesn’t strike me as the kind of guy to get emotional. If I had to guess, I’d bet that he was stone-faced in front of his computer screen, watching the ticker and robotically running calculations in an Excel spreadsheet.

So what does a serious guy like that do when he’s haemorrhaging money?.

If he’s as smart as everyone thinks he is, he probably recognises the fact that the money was never real in the first place.

I’ll get to it in a moment, but first we need to rewind to where it all started.

The hot factor

Facebook’s origins are surprisingly juvenile.

In 2003, Zuckerberg wrote a program that allowed his fellow students to compare two female students side-by-side and to choose which one was ‘hotter’.

He called it ‘FaceMash’.

That’s right…a company that’s worth about half a trillion dollars today was started to compare the hotness factor of girls.

By 2004, Zuckerberg’s service had expanded to Stanford, Columbia, Yale and other Ivy League schools.

By the end of 2005, Facebook had 6 million users.

Today, there are 2.23 billion users. That’s about 30% of everyone in the entire world.

Facebook’s financial path to the present was unique.

In its early days, Zuckerberg’s project was just that — a project — and the monetisation aspect was yet to be determined. Investors who backed Facebook before 2006 were gambling that one day, Zuckerberg would be able to convert user data and traffic into dollars.

One of the earliest investors was now-Kiwi, Peter Thiel. He put up $500,000 of capital in the summer of 2004 in return for 10.2% of the company. What an investment that was…

Within a couple years, Microsoft would buy a 1.6% stake for $240 million.

However, during all this time, Facebook was in the red. It was making some revenue through advertisements, but it wasn’t breaking even.

Only in September of 2009 did Facebook finally turn cash-flow positive.

In 2012, Facebook went public and raised over $16 billion, making it the third largest IPO in US history (behind General Motors and Visa Inc.).

Since then, the company has focused on acquiring tech start-ups to help diversify the platform’s capabilities. Think Instagram and Whatsapp.

The company is now worth $506.2 billion. [openx slug=inpost]

It doesn’t add up…

In a decade and a half, Facebook went from a dorm-room pet project to a company valued higher than the GDP of the bottom 175 countries in the world.

But the company’s cash flow isn’t even close to keeping up.

In 2017, it made $16 billion in profits on $40 billion in revenues.

That’s a drop in the bucket compared to most of the Forbes Global 2000.

Walmart, for example, made about $485 billion in revenues in 2017, compared to Facebook’s $40 billion.

But Walmart’s market cap is only $246 billion compared to Facebook’s $506 billion.

12x the revenue and ½ the market value?

It just doesn’t add up.

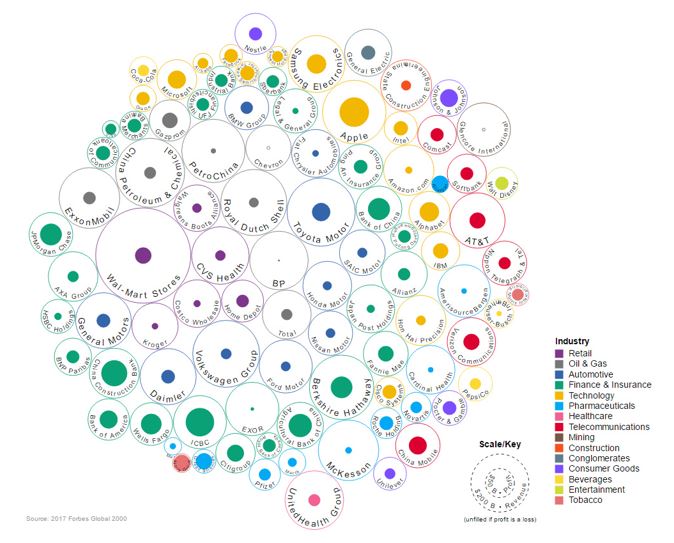

Take a look at how Facebook stacks up against the revenue and profit of top 50 companies in the world:

|

|

Source: Visual Capitalist |

If you can’t tell, Facebook is one of those tiny yellow dots at the top.

It barely even registers.

You’d expect the market caps of these companies to match the revenues…more or less.

But it doesn’t. It’s detached. Like a balloon untied from Zuckerberg’s wrist, Facebook has floated away into the wonderful world of mania.

Bang for your buck

Unlike your typical blue-chip companies, which are rooted to earnings to some degree, Facebook and its FAANG siblings are funded by the imaginations of their investors.

They believe that these companies hold potential…that one day, in the world of big data, Facebook will reign supreme.

I agree…somewhat. At this time, I don’t think anyone except maybe the NSA can compete with Facebook’s intimate user data.

While I appreciate Facebook’s potential, at some point, you need to value the stock. And to me, stock valuations come from real hard numbers, not faith.

You look at the earnings, profits, debt, development pipeline, etc., and you calculate a number.

If the shares cost more, it’s not worth it — it’s above your ‘walk away’ number.

You’d do the same thing for any other investment, wouldn’t you?

If you’re buying a car, you’d look at the resale value, repair costs, depreciation rate, etc., and determine if the asking price is worth it.

If it doesn’t add up, you don’t buy it. Simple.

And Facebook’s numbers don’t add up. So why are investors flocking to Facebook despite unrealistic stock prices?

Hope…that someday it can turn hype into profits.

It’s a gamble, but maybe investors will get lucky.

As Mr Jovi would say, ‘Take my hand, we’ll make it I swear. Livin’ on a prayer. Livin’ on a prayer’.

Best,

Taylor Kee

Editor, Money Morning New Zealand